Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

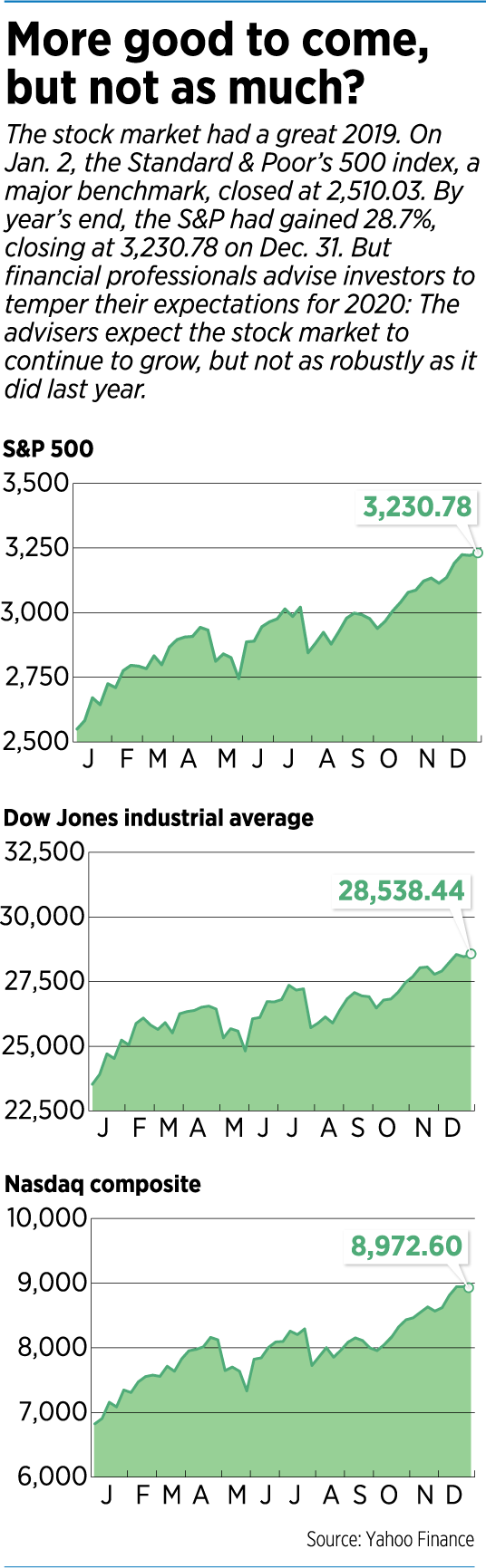

Investors couldn’t have asked for much more in 2019, as the decade-long economic expansion rolled on and stock indexes hit record highs.

Consider, for example, the Standard & Poor’s 500 index, a major benchmark. After some ups and downs earlier in the year, the S&P ended 2019 at 3,230.78, up 28.7%.

But don’t look for a repeat performance in 2020, local financial advisers say.

“As we come off of an incredible 2019 from a stock market standpoint, we’ll work with clients to temper some of their expectations for 2020 and beyond,” said Mike Green, complex manager for the global wealth management division of Morgan Stanley Smith Barney’s Indianapolis office. “Our belief is that the expansion will continue, but at a slower pace.”

While acknowledging that the current expansion cycle—already the longest in U.S. history—will end at some point, Green and the others say they don’t see signs of a looming recession.

“Even though we’re late-cycle, our house view still calls for the economy to grow at about a 2% rate for 2020,” said Jim Macdonald, the Indianapolis-based managing director for JPMorgan Private Bank in Indiana and Kentucky.

Consumers’ savings rates and balance sheets are strong, Macdonald said, interest rates are stable, and the financial system is well-capitalized.

“Those are all constructive signals for the economy to remain on a growth track,” he said.

Advisers offer varying ideas on how investors might position themselves for the year to come.

In recent years, Green said, investors have generally racked up good results with indexed funds because the stock market has been so strong overall. That’s not likely to be the case going forward.

“We believe that the markets will not, broadly, give us much in the way of returns,” Green said. “It means you have to be more tactical.”

Doing so, Green said, means using an active management strategy—researching and investing in particular stocks with the goal of achieving higher returns.

Doing so, Green said, means using an active management strategy—researching and investing in particular stocks with the goal of achieving higher returns.

“We think that constructing portfolios using active management has a better probability of performing well over the next few years,” he said.

Green declined to identify target companies or sectors, saying the ideal investment will vary based on factors like a client’s risk tolerance and financial goals.

Charlotte Lippert, chief investment officer at Indianapolis-based Valeo Financial Advisors LLC, said international stocks might be an area of opportunity.

For a variety of factors, including trade wars and a strong U.S. dollar, international stocks generally have lagged U.S. stocks over the last 10 years or so, Lippert said.

But over the next five to 10 years, that dynamic might flip, especially for companies in developing nations. “We don’t have the expanding middle class and income growth [in the United States] that some of these emerging countries have overseas.”

Burton Street, senior vice president and branch manager for Robert W. Baird & Co.’s Indianapolis market, offered a different view.

Rather than trying to maximize returns, Street said, investors should mostly focus on achieving a return that will meet their own goals. For investors who did well in stocks last year, that might mean moving money into high-quality fixed-income assets, such as bonds.

For an investor seeking a 7% return, for instance, “It only makes sense to reduce the risk. Even if the market’s up 25%, you don’t need to be up 25% to reach your financial goal,” he said. “If your goal is to try to beat the market every year, it’s extremely difficult.”

One wild card for investors will be the outcome of the U.S. presidential election.

“Regardless of why the economy’s doing well, the economy is doing very well right now. And a change of power. … That could kind of change the direction,” Street said. “So you need to pay attention to the election.”

Lippert has a different take.

“You might see some short-term noise around all of that, but in terms of long-term effects, the stock market tends to be driven by things other than the drama of politics,” she said.

No matter what the new year brings, Macdonald said, investors should avoid converting their investments to cash. Even if you fear a market downturn, he said, cash holdings are not the best idea.

“We don’t encourage clients to engage in market timing because no one has a perfect crystal ball,” Macdonald said. “It’s important to stay invested with consistency.”

Across multiple asset classes, including real estate, equities and fixed-income investments, “there’s only been one year since 2002 when sitting in cash was the best-performing thing you could do from a return perspective for the entire year,” Macdonald said.

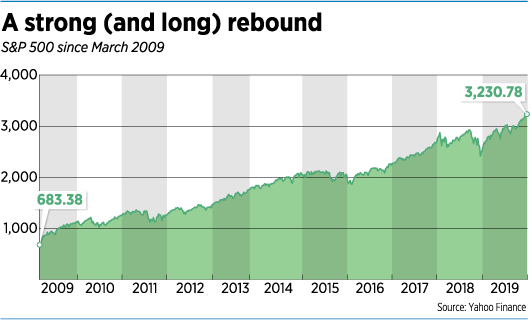

That year was 2008, when the onset of the Great Recession walloped stocks, sending the S&P 500 index down 38.5%.

Further, investors who hoard cash in a quest to miss the downside might not fully appreciate that they risk missing out on additional upside.

Further, investors who hoard cash in a quest to miss the downside might not fully appreciate that they risk missing out on additional upside.

The investment-research firm Crandall Pierce & Co. noted that, if you invested $10,000 in the S&P 500 on Jan. 1, 1969, then did nothing for 50 years, the money grew to $241,368 by the end of 2018.

But if you instead tried to time the market and missed just the single best day in each of those 50 years, you’d have had less than a fifth of that amount.

One thing all the advisers agree on: Having a good financial plan is crucial.

“We’re a planning firm first,” Lippert said. “So much of what we do is [to] try to have a broader picture beyond just the portfolio.”

That plan will look different for each client, Street said, but all plans will have some common elements.

Clients should choose financial goals—maybe saving for a child’s college expenses or building up retirement savings—then figure out the savings and return rates to achieve those goals. Good planning will also include tax strategies and insurance coverages, Street said.

Macdonald said clients should consider their financial plan a “living document” that they review and adjust as needed. “It’s a really great idea to look at that, minimally, annually.”

A financial planner can help clients map it all out, Green said. The planner can also serve as an accountability partner to keep a client on track. An adviser, for instance, might steer his or her client away from a tempting but ill-advised major purchase.

“Spending is a big part of the equation,” Green said.

Having a solid financial plan, Street said, also can help clients stay the course and avoid getting distracted by events of the day.

“If you don’t have a plan, get a plan and then stay disciplined and stick to the plan,” he said.•

Please enable JavaScript to view this content.

Editor's note: You can comment on IBJ stories by signing in to your IBJ account. If you have not registered, please sign up for a free account now. Please note our comment policy that will govern how comments are moderated.