Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

Higher interest rates are motivating more people to jump into the market for certificates of deposit, but area bankers and financial experts say it’s hard to predict how long rates up to 4% or 5% will last.

Part of the beauty of CDs is that today’s attractive rates are guaranteed for the full term of the CD, as long as no funds are removed before maturity.

Nationally, that is driving demand for CDs maturing in less than a year to a level not seen since the 2008 financial crisis, according to CUSIP Global Services. Local banks are experiencing the same rush.

“We’ve seen demand skyrocket over the last six months to the point that we’re selling 10 times the number of CDs we did in 2021,” said Michael Luebcke, Indianapolis district leader of Cincinnati-based First Financial Bank. “With lending rates doubling over the last 12 months, that’s spurred these deposits to increase.”

Those figures, he said, are true for Indianapolis-area branches and throughout First Financial’s system.

Now, stashing away $10,000 for 12 months at an annual percentage yield of 4.5%, for example, would bring in $450. A CD of $50,000 would produce $2,500 at 5% in a year. While a 12-month $2,000 CD with 3.5% APY would earn only $70, area banks are seeing more people dive into savings instrument with a broad range of deposits.

“With the low-interest-rate environment we had over the last several years, CDs sort of had fallen out of favor. With rising interest rates, they have become compelling once again,” said IBJ finance columnist Peter “Pete the Planner” Dunn.

But he said he doesn’t believe higher rates are on the radar of many millennials and younger adults, who aren’t as attuned to CDs since they haven’t experienced the higher rates. CD interest rates hovered just above zero for much of the 2010s and early 2020s; they haven’t been as high as they are now since 2008.

While interest rates have certainly driven the CD bandwagon, other factors might be at play.

Dunn stressed that CDs are more of a savings vehicle than an investment, because of their guaranteed return.

“There’s nothing really exciting about them. They are made to make you feel better, as opposed to investments that are more risky,” said Dunn, CEO of Your Money Line, which provides companies with financial wellness programs for employees.

Their current popularity, he said, might partly reflect today’s political landscape.

“We all suffer from political fatigue and anxiety,” he said. “When you’re able to protect your own money from that anxiety, that’s compelling. I think there’s value in that, for people who are anxious about other areas. With a CD, at least you know what you’re getting.”

Nationwide run

Whatever the reason, area bankers are finding a welcome audience for their growing number of CD products.

Consumers with wide financial backgrounds, Luebcke said, are buying First Financial’s CD products with initial investments ranging from $500 to $5,000 and varying maturity rates. He said a nine-month CD carries a 3.5% rate, while a 15-month CD offers a 4% rate with a $5,000 investment—the highest rates First Financial offers for short- and mid-term CDs now.

Luebcke said First Financial is reaching out to existing clients, using new “preferred banker” positions, to make sure clients get information about CD rates and the strategy of “laddering,” which spreads funds out over multiple CDs with varying maturity rates. The bank also connects customers with their investment experts, who can tell them about Treasury bonds and long-term financial strategies.

Nationally, many banks and credit unions are experiencing the same type of run on CDs. The run was precipitated by the Federal Reserve’s boosting its benchmark federal funds rate seven times last year, taking it from near 0% to a range of 4.25% to 4.5% in an effort to reduce inflation. This year, the Fed approved its first rate hike in February, raising the target federal funds rate to 4.5% to 4.75%.

The federal funds rate is the percentage banks charge each other for overnight loans, and changes in the rate affect borrowing costs for various financial products. CD rates correlate strongly with the federal funds rate. When it goes up, so do interest rates on CDs.

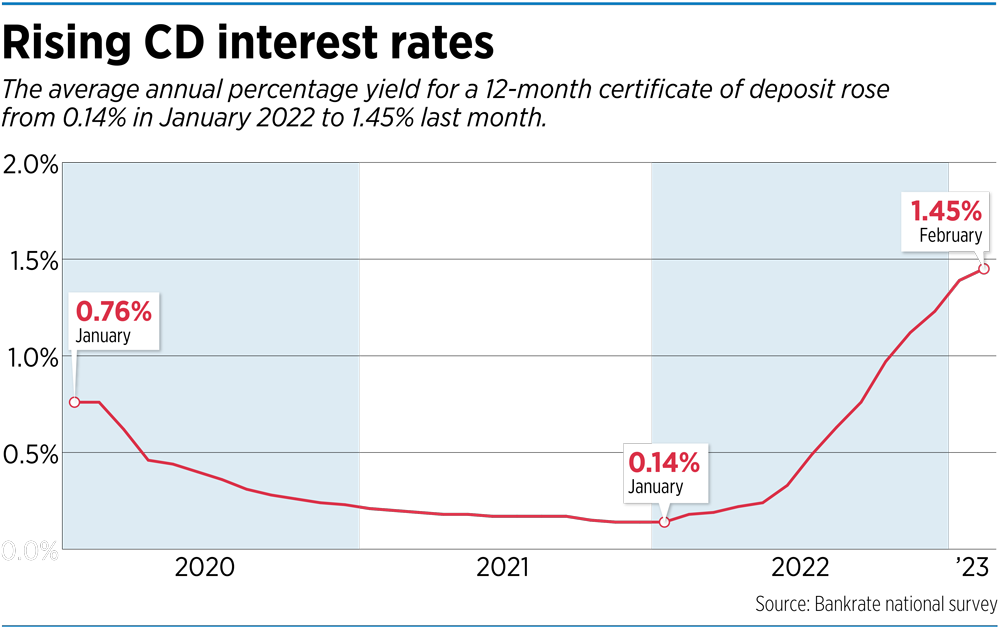

The increase in CDs’ average annual percentage yield indicates how much the market has changed. In January 2022, the average APY for a one-year CD was only 0.14%—a pandemic low, according to Bankrate.com. By February 2023, the average rate had risen to 1.45%.

And customers can find much higher rates just by shopping around.

A range of options

Brent Tischler, CEO of Community Banking at Old National Bank, said the bank is seeing widespread demand for CD products from customers across the financial spectrum because of the bank’s wide selection of CD products and the increasing public knowledge of today’s good rates.

“We’re seeing increases in both our money-market and CD categories,” he said, declining to be more specific. “Our CDs represent between 10% and 15% of our total community bank deposits.”

The bank uses customer and business deposits to help fund loans given in communities it serves, he said. “Growing deposits is among our highest priorities in 2023, to ensure we continue to fund our strong loan demand.”

Old National Bank offers a wide range of CD terms from six to 60 months, including multiple products with interest rates over 4%, according to Tischler. He encourages people to talk with their local bankers to find the savings and investment options best suited to them.

Steve Goodman, head of product for Consumer Bank of JPMorgan Chase, said the bank started raising CD interest rates last summer after testing the marketplace to gauge the demand at varying rate levels.

“The interest has been widespread across all different segments of customers, which is great,” he said. Bankers talk with customers about their financial needs and engage in a holistic conversation with them about all the bank’s products and benefits, Goodman said.

JPMorgan Chase also has seen increased interest in their CD products.

Right now, the bank is offering a 12-month CD for its customers at 3.75% APY for $100,000 or more deposits, 3.25% for $10,000 to $100,000, and 3% for up to $10,000. With a three-month CD, customers get 4% with a minimum $100,000 deposit, 3.5% with deposits of $10,000 to $100,000, and 2% for under $10,000.

“We’re always evaluating the rates we have out in the marketplace,” he said, noting the dynamic rate environment. “We want to have a competitive rate.”

When consumers are deciding whether to buy CDs, Dunn said, the biggest consideration should be how long they’re willing to forgo easy access to their money.

“If you have a $50,000 savings account, it’s unlikely you need all of that. If parting with $1,000 is a big deal for you, you probably don’t want to lock up the money for a year,” Dunn said. He advised that people generally keep liquid three to six months’ worth of expenses.

While CDs are nearly risk-free, experts agree it’s important for consumers to make sure their accounts are with a bank insured by the Federal Deposit Insurance Corp. or a credit union insured by the National Credit Union Association. Consumers who close out a CD before it matures, though, typically suffer some type of early-withdrawal penalty, such as loss of interest for a certain period.

Many financial experts expect more rate increases this year, as many believe the Fed rate will surpass 5% before trending lower in 2024 and 2025.

“I don’t think this is going to last incredibly long, maybe a year,” Dunn said. “In about 12 to 18 months, you might see rates fall again. “It’s a good time to get in and lock in a higher rate.”•

Please enable JavaScript to view this content.

Editor's note: You can comment on IBJ stories by signing in to your IBJ account. If you have not registered, please sign up for a free account now. Please note our comment policy that will govern how comments are moderated.