Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

Evansville-based Old National Bank is working on a first-of-its-kind effort: the launch of an Indiana-based bank whose target customers are minorities and those underserved by traditional banks.

The bank, to be called Generations Community Bank, would be based in Indianapolis and would be a for-profit business that’s open to all customers but designed to serve the city’s Black and Chin residents in particular.

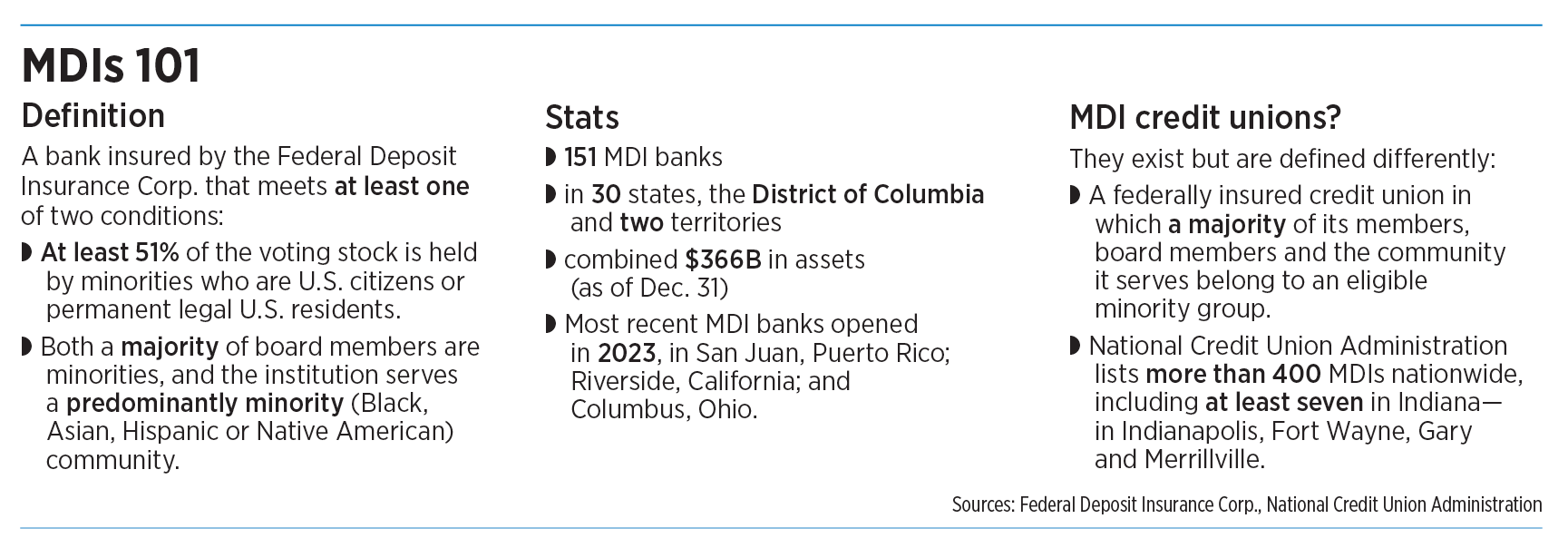

Old National is seeking minority depository institution status for Generations. This is a designation granted by the Federal Deposit Insurance Corp. for banks with at least 51% minority ownership or that serve a primarily minority community and have at least 51% of board seats held by minorities.

Banks with MDI status have access to certain federal funding sources, training and technical assistance that are not available to traditional banks.

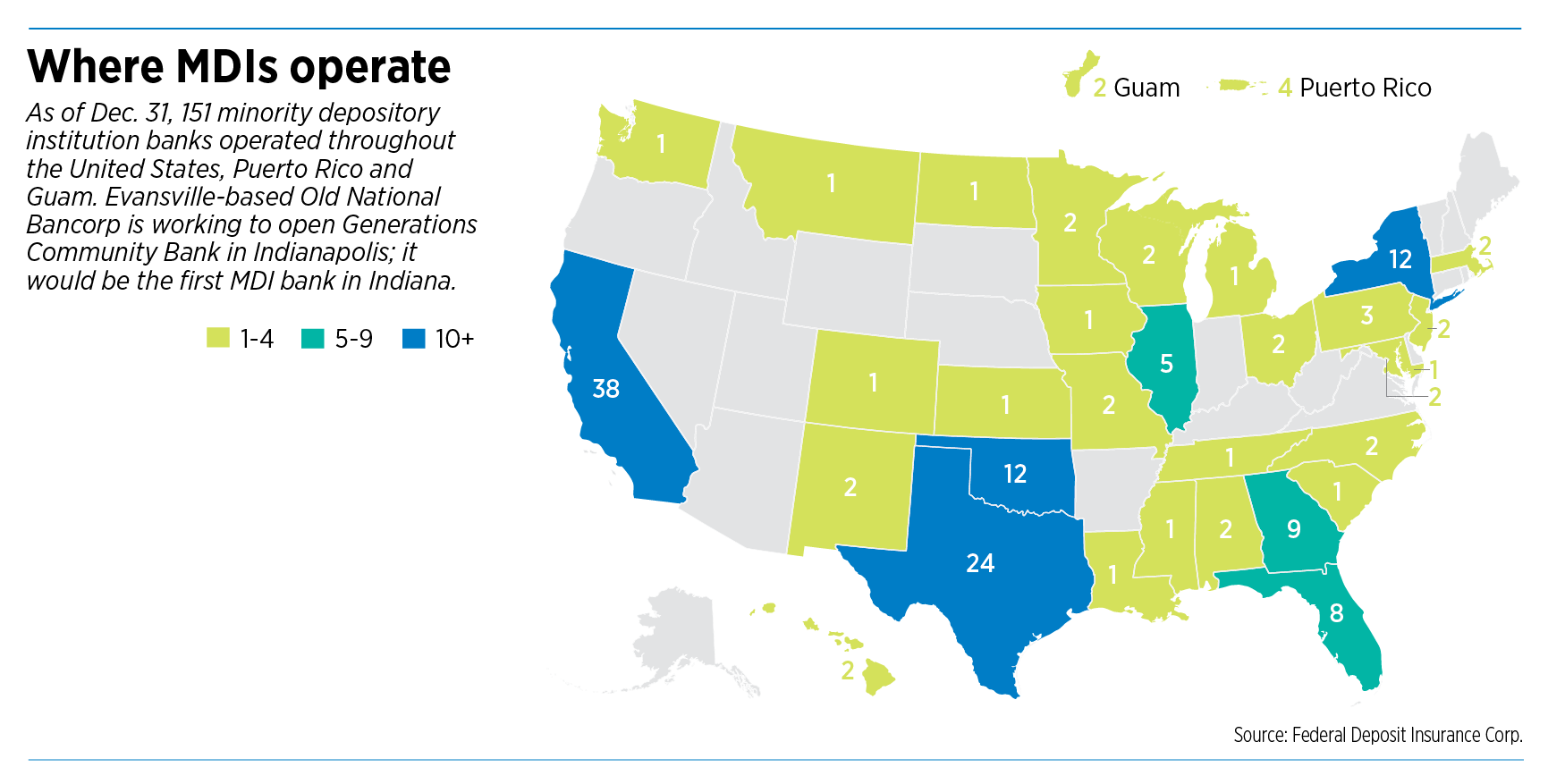

Only 151 MDI banks currently operate in the United States and its territories, and Generations would be the first in Indiana.

Old National’s Indianapolis market president and chief impact officer, Rafael Sanchez, who is leading the effort to launch the bank, said his research leads him to believe Generations would also be the first MDI in any state to be created by another bank.

“We’re treading new ground here,” Sanchez said.

The effort, which has been more than two years in the works, is still making its way through the regulatory approval process with both the Indiana Department of Financial Institutions and the FDIC.

The Indiana Department of Financial Institutions declined to comment on the status of the Generations application, citing the confidential nature of such information.

But Sanchez said the approvals process is moving forward—and if everything goes as planned, Generations will open for business by the end of the year.

Laying the groundwork

As part of the startup process, the work of soliciting investors will begin as soon as this month.

Sanchez said his goal is to raise at least $25 million from investors—ideally, $30 million. That investment will represent the bank’s initial asset base. Sanchez’s goal is to grow assets to $180 million by the bank’s third year of operations.

In banking, an institution’s size is typically measured by the value of its assets. As a point of comparison, Old National has $54 billion in assets.

Plans call for Generations to start out with two branches: one near the intersection of 21st and Illinois streets, and one inside the Baxter YMCA, just west of U.S. 31 between Southport and Stop 11 roads. The YMCA location is meant to serve the city’s Chin population, which is concentrated on the south side.

Sanchez has tapped longtime local bank executive Al London to serve as Generations’ CEO. London spent more than 20 years with J.P. Morgan Chase & Co. before joining Old National a year ago, with the plan that London would leave Old National for the top spot at Generations once that bank launched.

In moving to Old National, London left a job at America’s largest bank for a future position at a tiny startup that hadn’t even launched.

After considering Sanchez’s offer for about a year, London said he decided the risk was worth it.

“I get to establish a resource that will be here for generations to come, and it helps impact lives. So it became very clear to me that this was the right move for me and my family to join this mission,” he said.

The tie-in with the Chin community came through Rome Thalop, founder and CEO of Indianapolis-based construction, development and investment firm The Thalop Group Inc.

Thalop, who is active in local Chin community organizations, was part of a group that about two years ago decided it wanted to set up a Chin-focused credit union.

The effort and investment proved to be trickier than the group had anticipated, Thalop said.

“I didn’t know how challenging banking was,” he told IBJ.

A consultation with a banking attorney led to an introduction to Sanchez, who practiced law before joining Old National. After hearing about Generations, Thalop and his associates decided their better option was to team up with Old National rather than going it alone.

For the Chin community, Thalop said, Generations will serve several functions.

Most obviously, it will serve the lending and depository needs of the Chin community. But it could also provide financial education, especially in the area of investments.

In general, Thalop said, members of the Chin community are good at saving their money and diligent about repaying loans. But, he said, many don’t know much about investment tools like 401(k) accounts or Roth IRAs—and, especially if a language barrier exists, they might not have the confidence to ask a traditional banker about such things.

Narrowing the wealth gap

As its name implies, the new bank’s mission is to help underserved communities build generational wealth and achieve upward mobility.

According to the U.S. Census Bureau, the median household net worth in 2022 (including home equity) was $176,500—but that figure varies widely based on the race of the head of household. Among white non-Hispanic households, the median was $256,000. Among Hispanic households, it was $59,380. Among Black households, it was $31,250. The median for Asian households was $383,800.

Homeownership rates also vary based on race, Census figures show.

In 2022, 66.7% of white-headed households reported that some of their wealth came from equity in their own home. For Asian, Hispanic and Black households, those percentages were 59.3%, 47.8% and 40.5%, respectively.

As a mission-driven institution, Sanchez said, Generations will be positioned to address financial inequality in a way Old National and other publicly traded banks cannot.

A traditional bank, he said, must keep its shareholders happy by focusing on financial metrics. That means, for instance, that if a mortgage applicant’s credit score is too low, the bank will typically decline the customer and advise them to try again in six months.

But Generations, Sanchez said, will work with customers to help raise their credit scores. That might include helping them with a plan to pay down debt, for instance, or educating them on the fact that having too many credit inquiries will hurt their score.

“It’s that hand-holding that a traditional bank doesn’t really do because there’s no profit in that,” Sanchez said.

In other words, Generations will seek to earn a profit but at a lower rate of return than a traditional bank would.

Speaking generally, Sanchez said an investor in a traditional bank might expect to see returns of 10%-11%. For an MDI, those returns might be more like 5.5 % or 6%.

Generations’ approach to customer service sounds good to Shamika Anderson, president of the Near North Development Corp.

“I believe that this will go over really well,” Anderson said. “I’m excited about working with them.”

Affordable housing is one of the organization’s areas of focus, and Generation’s planned 21st and Illinois streets location sits within the community development corporation’s boundaries.

Near North’s territory is heavily residential. Even though several commercial banks are in or near the neighborhood, Anderson said, local residents could use additional options for mortgages and commercial lending.

“Some [residents] just need help navigating the financial dynamics,” she said.

An independent entity

Generations won’t be a subsidiary or affiliate of Old National—it will be its own separate business.

Old National has committed up to $7.4 million in seed capital to launch the bank. That investment will convert into an equity stake in Generations, Sanchez said, but Old National will own no more than 4.99% of Generations’ voting shares.

Old National will, however, have board representation at the bank.

Bob Jones, who was Old National’s CEO from 2004 to 2019, is coming out of retirement to serve as Generations’ board chair. London, Sanchez and two other past and present Old National executives will also serve on the board: Chief Strategic Business Partnership Officer Roland Shelton and former Chief Credit Officer Daryl Moore, who retired from Old National in 2022.

Other Generations board members include Kristin Mays-Corbitt, president and CEO of Indianapolis-based Mays Chemical Co. Inc.; Ersal Ozdemir, founder and chair of Indianapolis-based real estate firm Keystone Group and owner of the Indy Eleven soccer team; Stephanie Kim, chief administration officer at Carmel-based Telamon Corp. and president of Carmel-based Telamon Robotics; and Jimmie McMillian, chief diversity officer and senior corporate counsel at Penske Entertainment Corp.

In addition to London, Generation’s other senior leaders will include Chief Credit Officer Kyle Middleton, Chief Financial Officer David Bratton and Michelle Carrera, head of risk and compliance.

Startup statistics

As a startup, Generations will be distinctive in another way: It will be among a small number of banks to have launched in recent years.

According to S&P Global Market Intelligence, only 48 banks have launched nationwide since 2020. That number includes six launched last year, eight in 2023 and 16 in 2022. Those annual startup numbers are an improvement over the post-Great-Recession period—from 2010 to 2017, the United States saw only 10 new bank starts. But startup activity remains far below its peak of 1997 to 2008, when more than 500 banks were launched.

Zuhaib Gull, an S&P Global Market Intelligence analyst who covers the banking industry, said one reason for the slowdown is that banking regulations are much tighter now than before the Great Recession.

Another reason, Gull said, is that a huge number of banks failed or fell into financial distress during the Great Recession and the years that followed. This created an opportunity for investors who wanted to get into the banking business.

“Why go through the hassle of trying to establish a bank when you could just as easily enter the market by picking up one of the banks on the failed-banks list?” Gull said.

Of the 48 banks launched since January 2020, Gull noted, six have been MDIs.

Diversity-related issues have emerged as a hot-button topic under President Donald Trump, who, on his first day back in office Jan. 20, ordered federal agency heads to “take immediate steps to end Federal implementation of unlawful and radical DEI [diversity, equity and inclusion] ideology.”

New Gov. Mike Braun, as well, has been outspoken on the topic. One of his first officials acts in January was to order the closure of Indiana’s Office of Equity, Inclusion and Opportunity, which had been part of the Governor’s Office.

Regardless, Sanchez and London said they’re not worried that shifting political winds will derail their plans.

“We’re not a DEI bank,” London said. “We’re a bank.”

Even if the FDIC decided to discontinue the MDI program, Sanchez said, Generations will move forward.

“You can’t regulate mission—and so we’re going to still do what we’re going to do,” Sanchez said. “We’re going to help the community in the ways that we plan on helping the community, and that’s not going to change.”•

Please enable JavaScript to view this content.

Editor's note: You can comment on IBJ stories by signing in to your IBJ account. If you have not registered, please sign up for a free account now. Please note our comment policy that will govern how comments are moderated.