Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now I grew up in the days when Halloween was fun and safe. The only downside was that I had older brothers who made a point of trying to scare me—and they often succeeded. As an adult, I don’t need my brothers to scare me. I just need to think about the future of retirement in America.

I grew up in the days when Halloween was fun and safe. The only downside was that I had older brothers who made a point of trying to scare me—and they often succeeded. As an adult, I don’t need my brothers to scare me. I just need to think about the future of retirement in America.

A study by the Schwartz Center for Economic Policy Analysis at the New School finds that “inadequate retirement accounts will cause 8.5 million middle-class older workers and their spouses—people who earn over twice the official poverty line of $23,340 (if single) or $31,260 (if a couple)—to be downwardly mobile, falling into poverty or near poverty in their old age.”

According to a survey of retirees by Transamerica, “approximately 36% say their financial situation has declined since entering retirement.” It’s estimated that 5% of retirees will receive some financial support from their children.

The estimated median household savings of retirees (excluding home equity) is $75,000, the survey found. It found that 9% do not have any savings, 31% have savings of less than $50,000, and only 38% have savings of $100,000 or more.

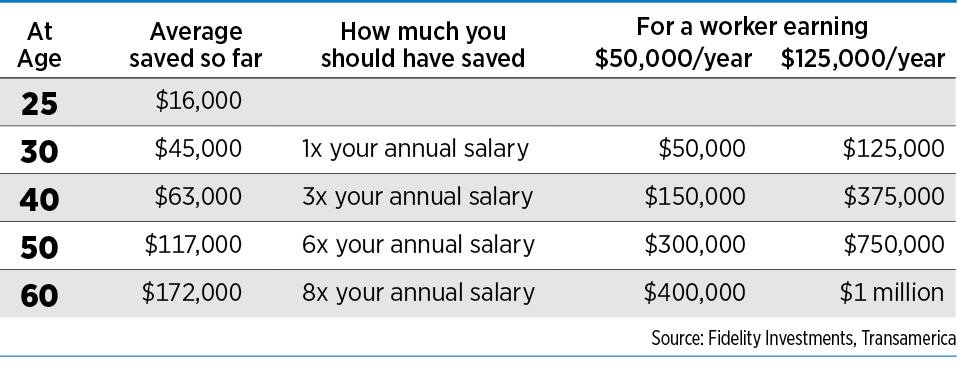

To the right is what the average American has saved vs. what financial experts recommend.

To the right is what the average American has saved vs. what financial experts recommend.

According to the Transamerica survey, retirees’ expectations for how long they will live are increasing.

The survey found the estimated life span of respondents was 90 in 2017, up from 86 in 2016. It found 49% are planning to live to age 80 and beyond, 32% age 90 or older, and 14% are planning to live to 100 or older. Let’s hope their health holds out that long.

According to the Insured Retirement Institute’s “Boomer Expectations for Retirement” survey, 70% are counting on Medicare to cover their health care expenses.

The reality, according to a report by Fidelity Investments, is that a retired 65-year-old couple can anticipate out-of-pocket health care costs of $275,000. A 2018 study by HealthView Services put the out-of-pocket number at $363,946. These amounts do not include the potential expense of long-term nursing care or rehabilitation.

The U.S. Department of Health and Human Services estimates that nearly 70% of people retiring today will require some type of long-term care during their lifetime.

In Indiana, the average cost for a year of long-term care in 2018 was $98,915. The IRI survey found 50% of respondents expect Medicare to cover the cost of their long-term care. The reality is that Medicare does not cover long-term-care costs.

Social Security will increasingly become the primary source of income for retirees.

According to a U.S. News & World Report article, “the average Social Security benefit was $1,461 per month in January 2019. The maximum possible Social Security benefit for someone who retires at full retirement age is $2,861 in 2019.”

Estimated median annual household income for retirees is $32,000, and 25% of retirees have a household income of less than $25,000.

It’s important to act now to try to ensure that retirement will be full of treats, not tricks.

Steps you can take now to improve your situation are to start or increase your savings amount, take advantage of employer retirement plans, calculate the cost of your retirement goals and put it in writing, and plan for the unexpected early retirement. And of course it’s smart to work to stay healthy.•

__________

Hahn is a certified financial planner and owner of WWA Planning and Investments in Columbus. She can be reached at 812-379-1120 or [email protected].

Please enable JavaScript to view this content.

Editor's note: You can comment on IBJ stories by signing in to your IBJ account. If you have not registered, please sign up for a free account now. Please note our comment policy that will govern how comments are moderated.