Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

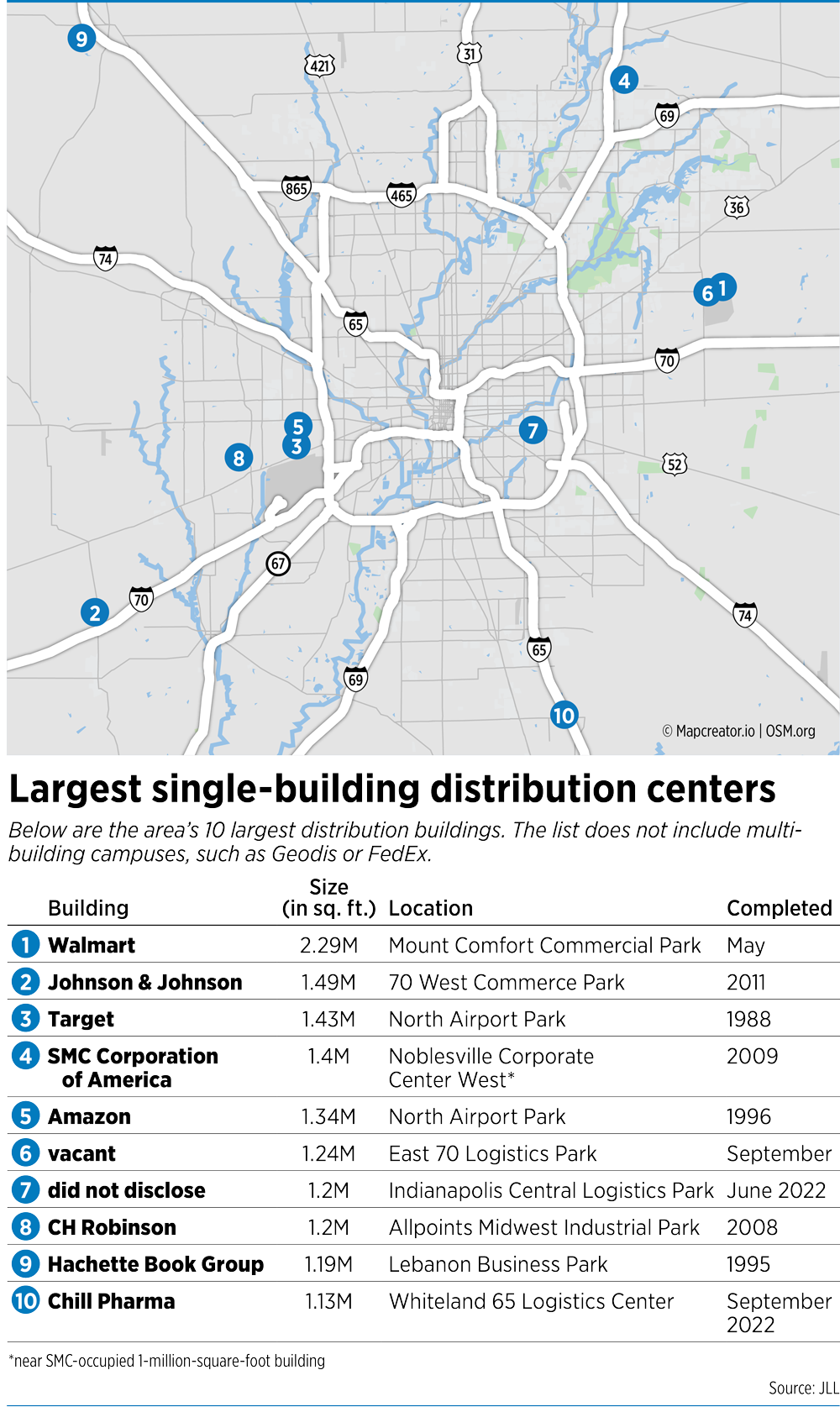

After riding a wave of strong development activity during the pandemic—including construction of the state’s largest distribution center to date with Walmart’s facility in the Mount Comfort corridor—central Indiana’s industrial sector is beginning to show signs of cooling off.

That slowdown in leasing activity, which began late last year, is putting some developers in a tricky spot as they try to fill massive buildings that either have recently come to the market or are under construction.

In fact, of central Indiana’s 27 modern distribution buildings of at least 1 million square feet, 10 have been delivered since 2022 and another three are on the way through mid-2024, according to data from the Indianapolis office of Chicago-based brokerage JLL.

What’s more, six of those buildings remain entirely empty, with brokers trying to secure users before the market flattens further.

That’s not to say there’s no demand for large-scale distribution centers. Rather, companies are simply reassessing their needs, in hopes of striking a balance between having a strong network of inventory-laden facilities and footing the bill associated with transporting and storing those goods.

“All of those buildings were built using historical data as justification for constructing facilities of that size—there’s been enough activity recently that it necessitated more 1-million-square-foot buildings for the market,” said Steve Schwegman, managing broker for the Indianapolis office of JLL.

“What’s happened, though, especially with interest rates creeping up, is that some of these occupants have pulled back on signing big lease deals. They’ve done all they can to lower their inventory levels, so that means they’re not out there looking for 1-million-square-footers. In fact, they’re trying to find ways that they can consolidate and shrink that footprint overall.”

Still in the works

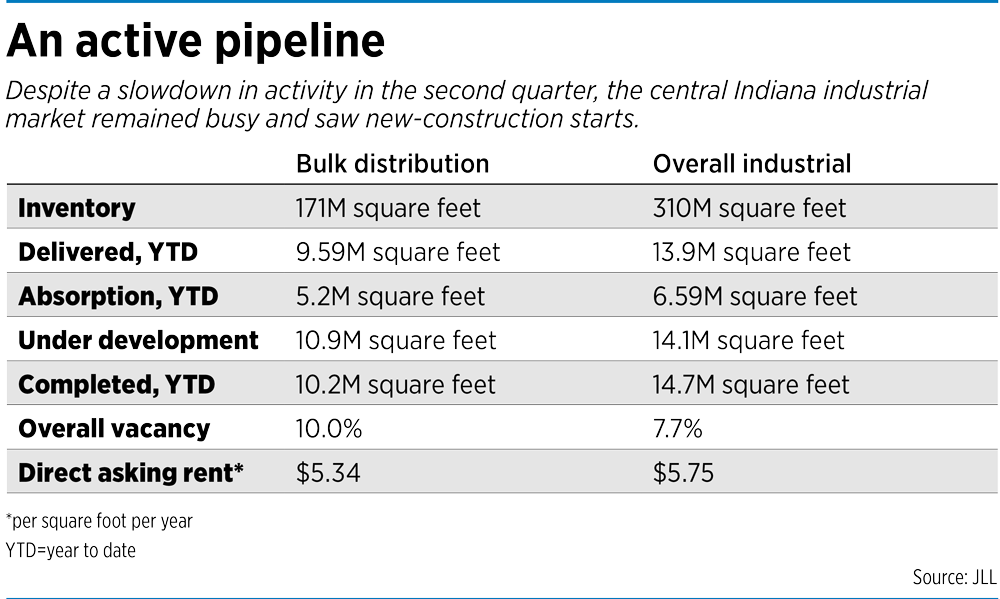

Through the second quarter of this year, more than 5 million square feet of new distribution space has been leased by the market. While experts said the continued absorption of that space is a good sign, it’s still a significant decrease from the same period in 2022—7.5 million square feet, according to JLL.

A large chunk of the absorption last quarter can be attributed to Walmart’s 2.29-million-square-foot facility by the Indianapolis Regional Airport in Greenfield. The three-story fulfillment center is one of the company’s largest in the world and could employ up to 1,000 people by the end of 2025. According to Walmart, the facility reduces the fulfillment process from a 12-step manual operation to only five instances where associates physically handle packages.

But despite companies like Amazon, Walmart, DHL and UPS taking out major space allocations in the past 12 months, the market continues to struggle with occupancy. Ten percent of bulk distribution facility space is vacant in central Indiana—the highest that figure has been in a single quarter since the start of the pandemic. It’s also a far cry from the 3.6% vacancy rate at this time last year.

So far in 2023, 9.6 million square feet of bulk distribution facilities has been completed, with another 10.9 million square feet under construction. In 2022’s second quarter, 22.2 million square feet of distribution center space was under construction.

Schwegman and other brokers said they expect the slowdown to continue, leading to fewer construction starts over the next 18 months. They also agreed that, because fewer large distributors still need the massive warehouses that have sprouted up across central Indiana in recent years, developers will be able to divide larger facilities to accommodate multiple users.

“You’re not going to see a lot of starts, save for a [few projects] here and there,” said Jeremy Woods, a broker in the Indianapolis office of Dallas-based CBRE. “The market’s going to go through a period where there’s a little bit of a lull in demand. That will pick up again at some point, but for now, it seems that the amount of space that the vast majority of occupiers have is serving them.”

Woods said the inventory of vacant buildings could be to the region’s advantage, as stragglers on the industrial side continue looking for space, both large and small.

“We’ve got a good amount of supply available and in the pipeline—and it’s crucial to have that, because when occupiers come into a market, they generally need space right away,” he said. “They don’t have time to do a build-to-suit project, so we were very well-positioned compared to our peers. We are going to attract an inordinate amount of that demand just because we have a readily available supply.”

Still in the works

In fact, there are still plenty of projects nearing the starting line and others just getting off the ground.

Carmel-based Lauth Group is building 2-million-square-foot Thunderbird Commerce Park on the site of the former Ford Visteon plant on the east side of Indianapolis, at 6900 English Ave.

And Ambrose Property Group, which pivoted to solely industrial development just months before the pandemic, is building out multiple sites across central Indiana, including in Monrovia and Mount Comfort. Last year, it completed a 1.2-million-square-foot building at the former Navistar site on the east side—just blocks from Lauth’s project—that is now fully occupied by an undisclosed user.

Stephen Lindley, Ambrose’s vice president of development and market officer for Indiana and Ohio, said it is “an interesting moment in time” for the industrial market both in central Indiana and across the Midwest, as some developers push ahead with new projects despite stagnation in lease-ups.

Ambrose has pumped the brakes on new speculative construction in Indianapolis, aside from what it’s already started. Among the projects it still plans to complete is a 1.03-million-square-foot structure at Monrovia’s Westpoint Business Park, where work got underway this year and is set to be finished by the end of 2024.

“Long term, we’re still incredibly bullish about the Indianapolis industrial sector,” Lindley said. “It’s been an incredibly resilient industrial market over the course of the last 20-plus years. It may take us a year, year and a half to lease up some of the vacancy that we’re staring at right now in our pipeline. But we still feel good about leasing demand in the market as a whole today and the number of users that are out there looking to occupy warehouse space” locally.

Dallas-based Mohr Capital Partners, which in 2020 announced plans for a 6.3-million-square-foot industrial park in Whiteland, is continuing to turn dirt on some of its larger buildings. Its Building 6 structure, which is 51% leased by DHL, is expected to exceed 1.05 million square feet by the time it’s completed this year. The remainder of the building is being marketed by CBRE.

Gary Horn, chief development officer for Mohr, said the firm is also mulling plans for another 1.2-million-square-foot building, although that one would be build-to-suit, rather than built on a speculative basis.

Not just Indianapolis

While Indianapolis isn’t a top 10 U.S. market for overall industrial space—it’s just outside, at No. 12, according to JLL—its abundance of single-structure distribution centers exceeding 1 million square feet is still among the highest in the country.

That doesn’t take into account more traditional manufacturing facilities like Rolls-Royce, Allison Transmission, Roche or Eli Lilly and Co. It also doesn’t factor in major campuses, like the 6-million-square-foot operation from logistics firm Geodis or the Fed Ex hub, both in Plainfield.

Michael Weishaar, an industrial broker with the Indianapolis office of Chicago-based Cushman & Wakefield, said even though Indianapolis has more large distribution buildings than most cities, peer markets like Columbus, Louisville and Chicago also have seen increases in bulk distribution construction.

“It’s not just an Indianapolis thing—these buildings are getting bigger and bigger,” Weishaar said. “I think something like the Walmart building is … an anomaly. But Columbus has a lot of 1-million-square-foot buildings that have gone up in recent years and so do these other peer cities. We might bode better in some situations, but it’s really tough, because every deal is looked at differently.”

In other regards, Indianapolis is hitting above its weight class. Last year, the area had seven of the top 100 transactions in the industrial sector, the sixth-best in the country. Chicago and California’s Inland Empire (Southern California east of Los Angeles) led that list with 11 and nine, respectively.

Larry Gigerich, executive managing director with Indianapolis-based site selection firm Ginovus, said statistics like how many bulk facilities a region has can be interesting and, in some cases, help inform would-be occupants of the network of activity for a given area. But the data is more about bragging rights than moving the needle, he said, because companies are more focused on location and ensuring a site is proximate to the rest of their distribution network.

“As we work on these projects for clients, so much of [their decision] is related to supply chain network, or … they’re trying to support an area geographically,” he said. “Now, certainly, [the Walmart distribution center] is a big project. … It’s certainly one that people can point to and say, ‘Hey, that’s a huge project.’ You don’t see very many of those.”

No more incentives?

One thing that often does play a role in bringing in new companies and development firms is incentives.

Mohr’s Horn said some submarkets, namely Boone County and Hancock County, are taking a more conservative approach to incentives than in years past. Both of those counties have seen massive investments from the industrial sector over the past several years and have now either effectively eliminated or greatly reduced the types of projects for which they’ll award abatements. That common tool, which usually lasts five to 10 years, helps occupiers save on personal and real property taxes.

Lebanon hasn’t offered traditional tax abatements for industrial development since Mayor Matthew Gentry took office seven years ago. Rather, it changed its strategy to look at front-loaded incentives like relocation costs or contributing to the cost of acquiring land. In many cases, though, no incentives have been offered.

Molly Whitehead, CEO of Boone County Economic Development Corp., said the shift hasn’t dissuaded companies from looking at Lebanon and has allowed the city to be more selective in who lands in town—with a focus on building stronger bonds with companies that locate there. Tax abatements are usually awarded to developers, who then control which tenants fill their projects.

Lebanon also is home to Indiana’s first LEAP innovation district, which is expected to encompass more than 9,000 acres. Hefty incentives are expected to be associated with any developments that go there (Eli Lilly and Co., the first tenant in the district, is receiving more than $270 million in tax rebates through a new state innovation development district designation, which acts in a manner similar to tax-increment-financing districts.) All incentives for LEAP are expected to be funneled through the Indiana Economic Development Corp., in partnership with Lebanon and Boone County officials.

Whitehead said Whitestown is exploring whether it can offer incentives only for companies that are expanding their presence in the area or for massive speculative industrial buildings, such as those exceeding 1 million square feet.

“That’s something we’ll continue to work with the town to determine what it is they want to see and gain from an economic development perspective and how we can help them get there,” she said. “Sometimes incentives are helpful, but maybe not all the time. So it’s something we’ll examine.”

Taking an approach less focused on the traditional abatement formula, Horn and other developers said, makes future distribution-focused industrial construction much less likely for Boone and Hancock counties, despite the heavy influence industrial projects have had on the growth of those communities in recent years.

Many central Indiana governments continue to offer abatements. This includes Indianapolis, which in June approved a $7 million abatement for a new industrial park at South Arlington Avenue and County Line Road. •

Please enable JavaScript to view this content.