Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now The following is an excerpt from Kirr Marbach & Co.’s first-quarter client letter, available at www.kirrmar.com.

The following is an excerpt from Kirr Marbach & Co.’s first-quarter client letter, available at www.kirrmar.com.

Conventional investment wisdom is, stocks are “risky” and bonds are “safe.” Owning stocks is exciting—you can make or lose a bundle. Bonds are boring—you don’t make much, but you can’t lose money, either.

Governments and corporations borrow by issuing bonds, which are a contract between the borrower and lender spelling out the timing and amount of interest to be paid (the “coupon”) and when the principal amount borrowed is to be repaid (the “maturity”). Because the amount and timing of the cash flows are contractually set, bonds are referred to as “fixed income” investments.

Although the cash flows are fixed by contract, the price of a bond will fluctuate based on interest-rate risk and credit risk.

Although the cash flows are fixed by contract, the price of a bond will fluctuate based on interest-rate risk and credit risk.

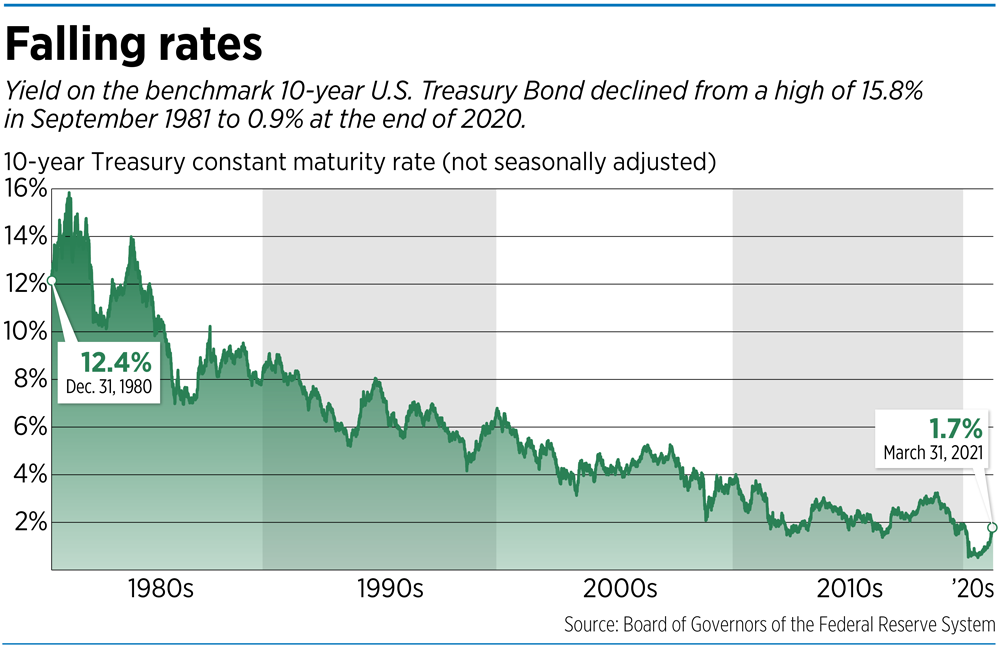

For the past 40 years, the conventional wisdom has been generally correct. The graph below shows the yield on the benchmark 10-year U.S. Treasury Bond (UST) declined from a high of 15.8% at the end of September 1981 to 0.9% at the end of 2020. Mortgage rates track the 10-year UST, so that’s why U.S. homeowners have benefited from both the lowest rates in history and the related surge in property values.

When interest rates are falling, a borrower can offer new bonds with a lower coupon than the higher coupons on bonds issued in the past, making the fixed-income stream on existing bonds more valuable and causing bond prices to go up. Conversely, when rates are rising, existing bonds go down in price. Thus, bond investors have enjoyed a glorious, mostly uninterrupted bull market the past four decades. Sweet!

Additionally, since the end of the Global Financial Crisis (GFC) in 2009, investors have pulled $780 billion from U.S. stock funds (ironically during one of the greatest bull markets for stocks of all time) and put $2.8 trillion into U.S. bond funds.

Unlike stocks, there is no upside beyond receiving the contractual payments. Credit analysis determines whether you’re being paid enough to compensate you for the risk that the issuer might default. The higher the credit risk, the higher the interest rate you should demand. For U.S. corporate bonds, this compensation is expressed as the interest rate “spread” vs. the comparable maturity UST (considered a “risk-free” credit because the government can always print more money).

Bonds rated “investment grade” by the three primary U.S. credit rating agencies (Standard & Poor’s Global Ratings, Moody’s and Fitch Ratings) traded at spreads as wide as 6% during the GFC, 4% during last year’s COVID panic and currently a tiny 1%. Similarly, “non-investment grade” or “junk” bonds traded as wide as 20% during the GFC, 9% last spring and now about 3.4%.

Bond investors will learn when they open their March 31, 2021, account statements that the conventional wisdom is sometimes wrong (even after 40 years), as the yield on the 10-year UST jumped to 1.7% on March 31, leading to a loss of 4.6% for the overall UST market for the quarter, according to ICE Indices. Further, USTs maturing in more than 15 years lost a whopping 13%. This was the worst quarterly performance for the UST market in more than 40 years.

It shouldn’t be unexpected or surprising that sub-1% yields were unsustainable in light of a U.S. economy setting up for a post-COVID recovery and trillions in stimulus and infrastructure spending that will have to be funded by the government’s issuing bonds.

Until recently, bond investors have enjoyed the best of both worlds as yields on USTs marched steadily lower and credit spreads contracted. With yields and spreads at historic lows and mathematically highly unlikely to go lower, investors are facing a lot of risk with little reward.•

__________

Kim is Kirr Marbach & Co.’s chief operating officer and chief compliance officer. He can be reached at 812-376-9444 or [email protected].

Please enable JavaScript to view this content.