Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe NowIndia Brown had no interest in getting a loan for her business.

The founder of Carmel-based consulting firm PM Phase, Brown started out her career in the financial services side of health care at Ascension St. Vincent in Indianapolis. In 2013, she took a chance and started her own company, which focuses on organizational and financial consulting.

But despite her work in finance, Brown said she felt hesitant applying for a loan to increase her staff.

“I was concerned that the business wasn’t as successful as I thought it was because I wasn’t sure if I had true visibility on where the finances were,” Brown said.

She’s not alone. Experts say the hesitancy of Black business owners to borrow stems from historical neglect of those customers by traditional banks—an opinion backed by extensive historical research.

Now Marshawn Wolley, CEO of Black Onyx Management and an organizational consultant for Black-led loan fund Equity 1821, has been working with banking partners to measure the problem locally and to educate borrowers about interacting with financial institutions.

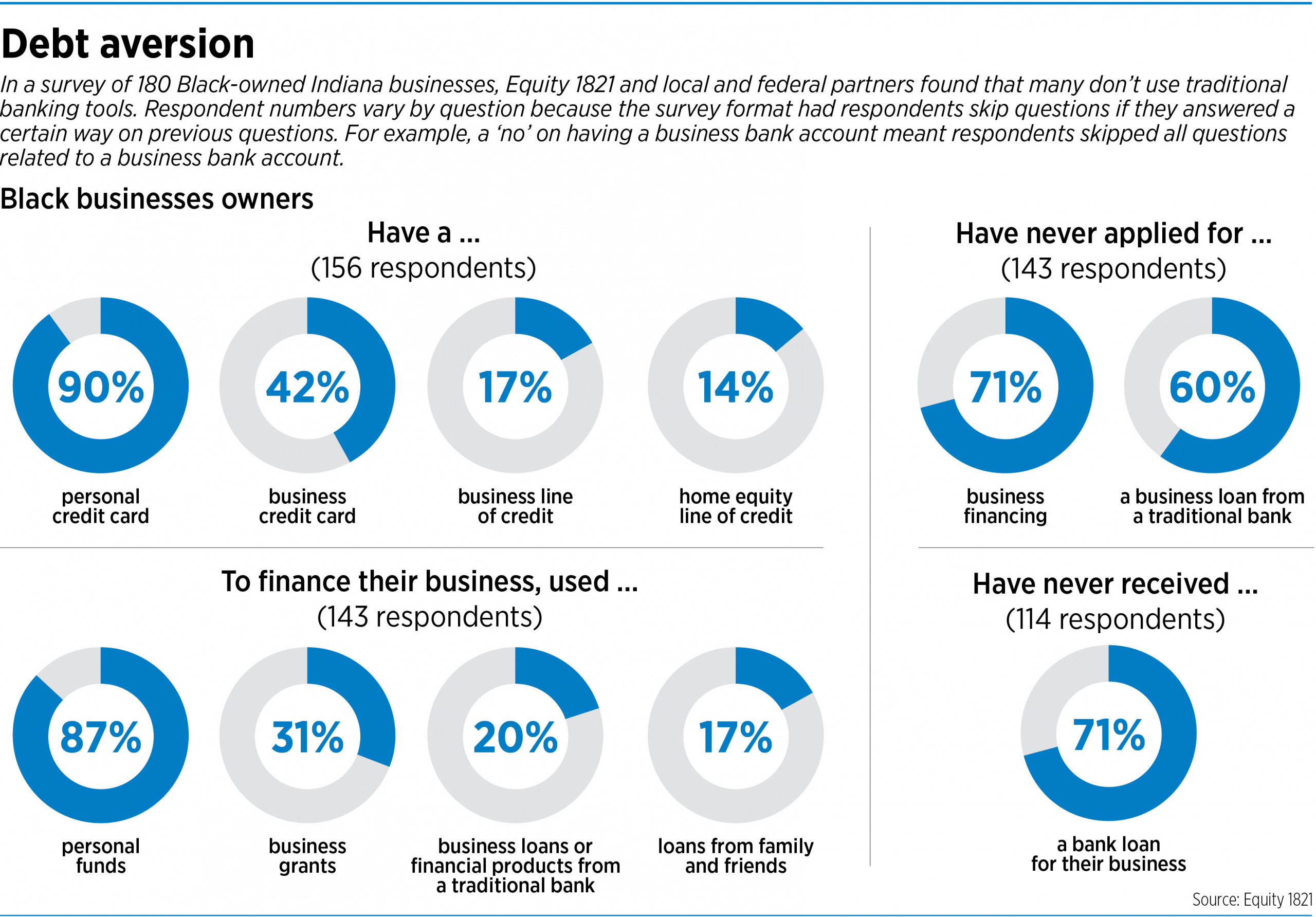

Brown was a participant in Wolley’s project, Demystifying Underwriting, which he’s been implementing with support from Columbus, Ohio-based Huntington Bank and the Chicago Federal Reserve. The project included a survey of 180 Black-owned businesses in Indiana and an in-depth focus group and training program for customers and banks. Since that study took place, Wolley has presented the results to a class at Harvard University and to the nation’s largest credit union association.

The survey found reluctance among Black business owners to acquire debt from traditional banks. For example, less than half of the respondents reported having a business credit card, less than 20% had a business line of credit and nearly half had no relationship with a primary banker.

The results weren’t surprising to other local leaders who aim to uplift Black business owners. Emil Ekiyor, founder and CEO of InnoPower, a not-for-profit that aims to connect Black business owners with resources, said the scarcity of bank branches in predominantly Black communities contributes to the discomfort with banks.

“You can drive down [East] 38th Street, from 38th and Meridian all the way to German Church [Road], you might not see that one bank,” Ekiyor said. “So it doesn’t become part of a community, part of a culture, where those things are prevalent.”

A 2021 report from the Washington, D.C.-based Brookings Institution found that not only do Black neighborhoods have fewer banks, but the impact of banking is different than in majority-white neighborhoods. “Interest rates on business loans, bank branch density, local banking concentration in the residential mortgage market, and the growth of local businesses are markedly different in majority Black neighborhoods,” the report said.

Deep roots

Economists say a long history of mistreatment by banks has left scars on the Black community that have been passed down through generations.

Ashlyn Aiko Nelson, an economist at IUPUI’s Paul O’Neill School of Public and Environmental Affairs, has studied the effect of race on banking with a focus on home and mortgage lending.

Under President Franklin D. Roosevelt’s New Deal programs enacted in the 1930s, the Public Works Administration created segregated public housing that was maintained and enforced by state and local governments that administered the public housing projects, Nelson said. When the Homeowners Loan Corp. launched in 1933, it gave low-cost mortgages to whites only. In 1934, the Federal Housing Administration was created; in its underwriting guidelines, it classified housing in Black or integrated neighborhoods as a poor risk.

That practice became known as redlining, Nelson said. The term is more colloquially used today to refer to the practice of denying mortgages to Black borrowers.

“Sort of as a result of this exclusion from the mortgage market, Black Americans are disproportionately less likely to have the types of intergenerational wealth transfers enjoyed by white families,” Nelson said.

She said the practices of the 1930s were “completely exclusionary, racist practices” that prevented communities of color from entering the formal banking sector. “And I think rightfully so, there is a lot of distrust of banks, formal lending institutions,” Nelson said.

What progress is made can become overshadowed. A December 2023 analysis by CNN found that Navy Federal Credit Union, the largest credit union in the United States, had the widest disparity in mortgage rates charged to white and Black borrowers of any major lender.

Wolley said that kind of news creates distrust among diverse business owners. Demystifying Underwriting aims to bring “culturally competent” information to banks and their users to both address the concerns of business owners and educate financial institutions about issues facing the Black community.

“That’s the reason why Black institutions matter, because we will ask these questions that maybe other institutions don’t either think to ask, or just it’s not part of their mission,” he said.

Turning the tide

Black-run organizations in Indianapolis have been trying to reverse the trend in which business owners use mostly personal finances to fund their business, a practice known as bootstrapping. But the results of Equity 1821’s survey showed it’s still common.

About 70% of respondents said they’d never received a business loan, and about the same percentage reported never having applied for any business financing. Of the 83 business owners who said they never applied for a bank loan, 29 did not want to accrue debt and 20 did not think their loan application would be approved.

According to a report released by the Federal Reserve in 2020, 80.2% of white business owners receive at least a percentage of the funding they request from a bank, compared with 66.4% of owners who are Black, indigenous or people of color.

When those minority-owned businesses do receive funding, it tends to average $30,000 less than comparable white-owned businesses, the Federal Reserve found. That feeds the cycle in which Black-owned businesses feel discouraged about seeking loans. The Fed found 37.9% of Black entrepreneurs don’t apply for loans because they believe they will be turned down; only 12.7% of white business owners feel the same.

Wolley hopes to improve those impressions with Demystifying Underwriting. With Brown as one of a dozen participants, Wolley worked with bank leaders from Huntington to teach Black entrepreneurs more about the loan application process and to study the problem of debt aversion on a more personal level.

Using a core group rather than one-on-one meetings with bankers created a more comfortable environment, Wolley said, which led to progress for Brown.

From 2017 to 2023, she had experienced “major growth” in the number of clients seeking project management work. Through her Demystifying Underwriting sessions, Brown realized she needed two additional full-time employees. She applied for—and received—a loan that allowed her to hire those employees.

“I did a complete overhaul of all of my financial documents with my accountant and set expectations with her based on [the] workshops,” she said.

Scott Ransburg, market president of Huntington National Bank, told IBJ the program was eye-opening for bankers, too, because he didn’t know so much aversion to traditional banks persisted among Black Hoosiers.

“It’s an education process, really, for us,” Ransburg said. He and other Huntington employees gave the group of entrepreneurs that participated in Wolley’s program insight into what bankers look for in loan applications.

Huntington said its work reaching out to local Black entrepreneurs is an extension of an effort the bank created out of the pandemic, called “Live Local,” where it invested $2 billion. The program provides small businesses with loans ranging from $1,000 to $150,000 with no fees and less restrictive credit requirements. It loaned more than $100 million in three years, surpassing a goal of that amount in five years.•

Please enable JavaScript to view this content.

Someone please explain to me how capitalizing one race but not another is anything but racism.