Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe NowA December 2025 deadline might seem far away—but for those who qualify for the estate-tax provision of the Tax Cuts and Jobs Act, now’s the time to decide whether and how to reduce the size of their estates.

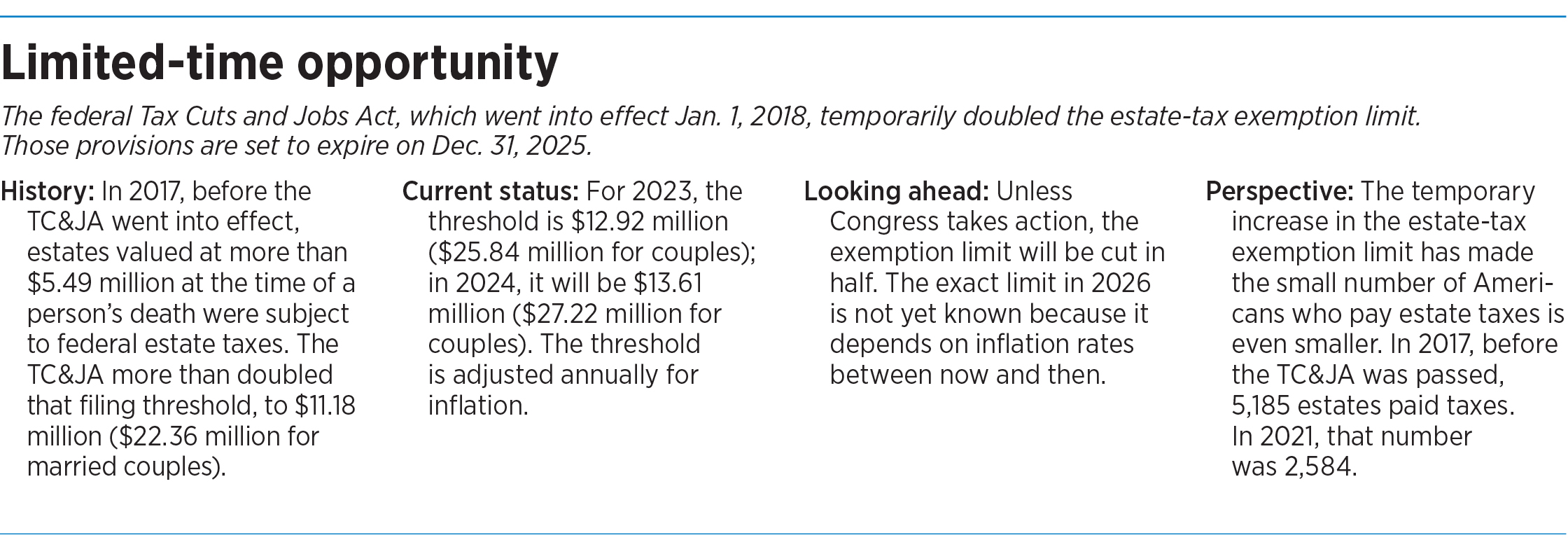

The TC&JA, which passed in 2017, temporarily doubled the estate-tax exemption starting in 2018. Right now, individuals can transfer up to $12.92 million to their beneficiaries (married couples can transfer up to $25.84 million) before triggering estate taxes. But the estate-tax provision of the TC&JA is scheduled to sunset at the end of 2025; barring congressional action, the exemption will be cut in half.

Granted, it’s an issue that’s relevant only to the wealthiest among us—a tiny fraction of the U.S. population. But for those who are in this group, reducing their estates before the exemption amount drops on Jan. 1, 2026, can offer big financial benefits. Estate taxes are levied on the portion of an estate that is above the exemption amount. That tax rate varies depending on the taxable amount of the estate, topping out at 40%.

For those with large estates, the TC&JA has offered a “generational opportunity,” said Gary Hirschberg, CEO and founding member of Aaron Wealth Advisors. Based in Chicago, Aaron recently opened an office in Carmel.

Asked to name a similarly meaningful opportunity, Hirschberg pointed to a circumstance that happened in 2010, when, because of congressional inaction, the estate tax lapsed for a year. As it happens, New York Yankees owner George Steinbrenner died in 2010 with an estate worth an estimated $1.1 billion. If the estate tax had been in place when Steinbrenner died, his inheritors would have been on the hook for an estimated tax bill of $500 million to $600 million, The Wall Street Journal reported at the time. But because Steinbrenner died in 2010, they paid no estate taxes at all.

Because it takes time to decide on a plan of action and put it into place, financial experts say it’s wise to get started now.

“These plans are complex, they’re nuanced, and they need time to be implemented correctly,” said Kristen Mallory, senior trust officer at Merrillville-based Centier Bank. “You don’t want to miss your opportunity to have taken advantage of this situation.”

A bit of technical explanation and background: In 2017, the estate tax exemption was $5.49 million per individual and $10.98 million for married couples. The threshold is adjusted annually for inflation. Because of the TC&JA, as of Jan. 1, 2018, the exemption doubled, which brought it to an inflation-adjusted $11.18 million for individuals and $22.36 million for married couples. The exemption increase was written to sunset after eight years, which will be Jan. 1, 2026.

It’s too early to say exactly what the limit will be in 2026, because it depends on inflation rates between now and then. But the IRS recently released its 2024 estate tax exemption, which will be $13.61 million ($27.22 million for couples).

Local financial professionals say they’re already having conversations with their clients about maximizing the advantage of the TC&JA’s estate-tax provision while it lasts.

“We’re really trying to get out in front of our clients now,” said Stephen Schnelker, a director in Indianapolis-based accounting firm Katz Sapper & Miller’s tax services group. Schnelker is a certified public accountant, and he also has a law degree.

Anyone whose estate is worth more than the expected 2026 exemption level—about $6.5 million for an individual or $13 million for a couple—should talk with their advisers about the upcoming change, Schnelker said.

“It’s just worth having a conversation now, rather than waiting until 2025, because there might be things that we can do now that might not be available if we wait too long,” Schnelker said.

The general goal is to move assets out of the estate now, reducing the amount that will be subject to estate taxes upon the estate owner’s death.

Perhaps the simplest option is to give the money away.

“If you give something sooner, and it continues to grow, then that growth outside of your estate benefits your family. But you’re not having that growth inside of your taxable estate to deal with later,” said Charlotte Lippert, head of family office services at Carmel-based Valeo Financial Advisors LLC.

But people who choose this option need to carefully consider how much they can afford to give. The issue is especially relevant to people whose estates are worth about $15 million to $40 million, Hirschberg said, because, if they use their full estate-tax exemption now by giving the money away, they might not have enough to sustain their current lifestyle.

“The one big mistake people do is, they give away too much money,” he said.

To address this concern, one popular estate-planning tool is the spousal lifetime access trust, also known as a SLAT.

Using a SLAT, one spouse sets up a trust for the benefit of the other and their children. Moving assets from the estate into the SLAT reduces the size of the estate while also giving the couple continued access to their assets.

Using a SLAT can help people overcome the psychological barrier of giving away assets outright, Schnelker said. “It’s a security blanket.”

On the downside, he said, setting up a trust requires time and expense. And there’s always the danger that the beneficiary spouse will die first, leaving the couple’s children—but not the surviving spouse—with access to the trust.

Many variables are at play when deciding on the best estate planning strategy, experts say.

Those factors include things like the age, health status and living expenses of the estate-holder. But they also include the type of assets held in the estate, whether they be stock holdings and retirement accounts or less liquid assets such as real estate or business interests. Family dynamics also come into play—how much of the estate should go to heirs and how much to charitable causes? Should parents leave differing amounts to different children based on each child’s own finances or life situation?

“Each client’s situation is very different,” said Erin Shaw, a market manager of the Indiana and Kentucky offices of J.P. Morgan Private Bank. “It’s not a one-size-fits-all.”•

Please enable JavaScript to view this content.