Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe NowCarmel resident Theresia Paauwe, a veteran of the central Indiana real estate market, bought her first home at age 18 in 1977. She bought her 10th last December (she sold her previous residence in February). Having watched interest rates rise and fall over the last six decades, she’s somewhat bemused by people who balk at paying 6% to 7% today.

“It didn’t scare me to come into this market and buy,” Paauwe said. “I think the highest rate I ever paid on a house was my first one in 1977. It was around 13%, and we didn’t bat an eye. That’s just how it was. I think people just got so used to those 2[%] and 3% rates that they thought it was going to last forever. When you have a longer view of it, you know that’s not realistic.”

Many of today’s buyers can expect a continued dose of that realism this spring, as the weather warms and residential real estate’s busiest season kicks into high gear. Experts say this year will see a continuation of the same pattern that’s governed the market since before the pandemic—too many buyers chasing not enough listings—with higher interest rates complicating the picture.

“We think the housing market will see the traditional, seasonal increase in sales activity,” said Shelley Specchio, CEO of MIBOR Realtor Association. “However, it is likely that stubbornly high interest rates will have a moderating effect—certainly compared to the previous three years.”

That could be especially true for younger buyers, who have never known anything except mortgages with interest rates so low the loans were practically free. Higher interest rates and fears about an economic downturn have combined to make raising a down payment and covering higher monthly mortgage bills more challenging or just scarier.

“We now have two generations, millennials and Gen Z, coming into the stages of their lives where they are looking to buy their first or even their second home,” Specchio said. “They’ve grown up in an economy where mortgages have largely been under 6%. There’s been a psychological effect of watching mortgage rates rapidly move from 3% to 7%,” the approximate current rate.

That sticker shock sidelined many potential buyers during winter, while at the same time prompting potential sellers to hold onto their properties rather than list them. Because if you’ve locked in a 3% mortgage on the house you already own, and you don’t have to move, why trade it in for a house with a (potentially) much higher monthly payment?

That sticker shock sidelined many potential buyers during winter, while at the same time prompting potential sellers to hold onto their properties rather than list them. Because if you’ve locked in a 3% mortgage on the house you already own, and you don’t have to move, why trade it in for a house with a (potentially) much higher monthly payment?

Still, Specchio said, there’s plenty of demand within the market, and sales could pick up.

“We expect 2024 to be a better year than 2023 in terms of sales volume, and [it] will likely seem more like pre-pandemic market levels,” she said.

Facing facts

Experts say that’s in part because buyers and sellers are accepting the fact that the higher rates aren’t going away anytime soon.

“We’re seeing closed sales running ahead of last year,” said Chris Watts, president of public affairs for the Indiana Association of Realtors. “But perhaps more importantly from our perspective, we’re seeing more folks venturing back into the market and considering selling their homes.”

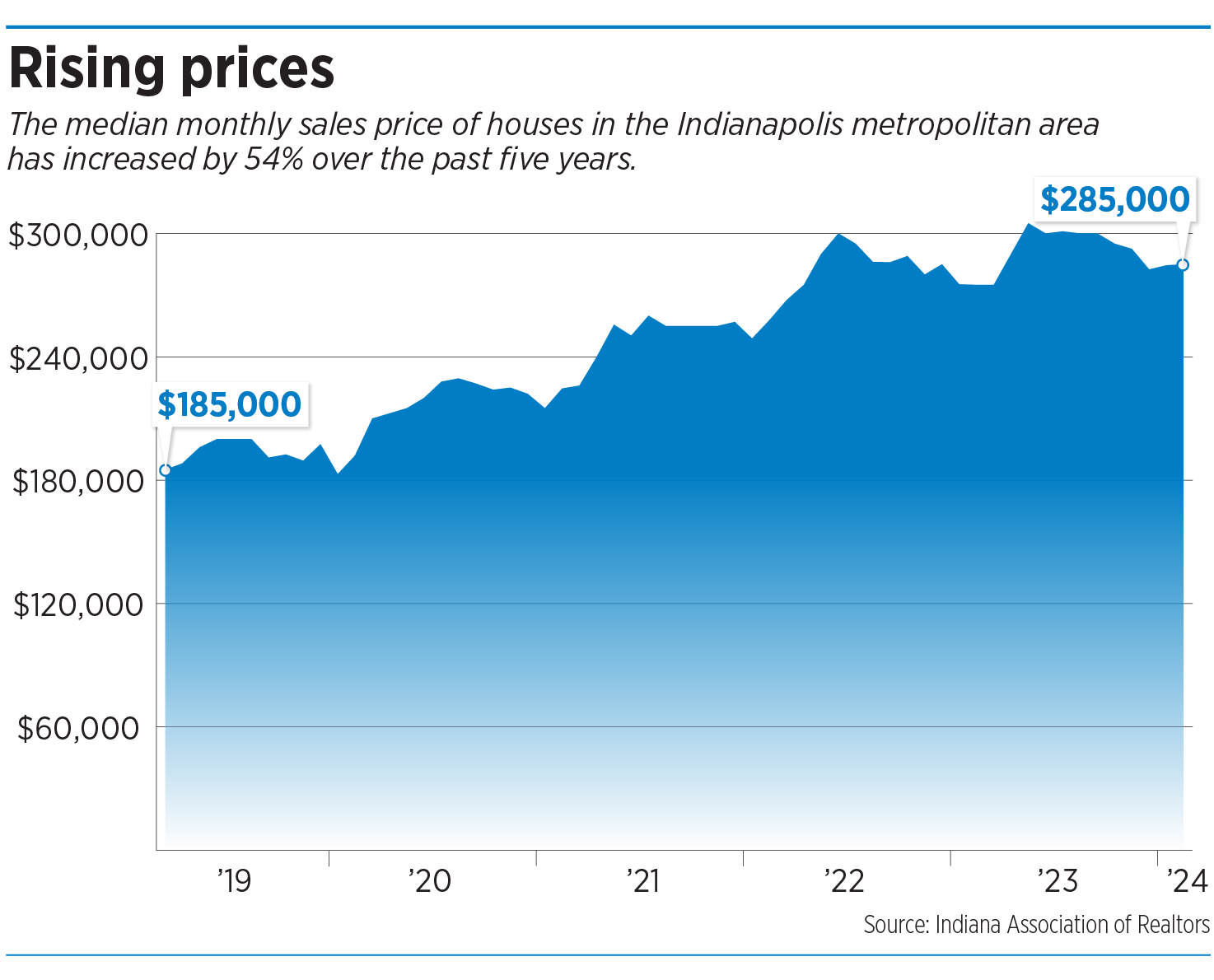

According to the association’s statistics, during February, 6,499 homes were newly listed statewide, a 10% bump from January and up 13% from last year. Indiana’s statewide median home price reached $238,000 in February (3% above the same month last year), with homes selling for 95% of original list price.

The median sales price for the Indianapolis metro area in February was $285,000, and $230,000 for Marion County.

“After a year of high interest rates and cool demand caused homeowners to postpone plans to sell, 2024 is seeing more properties hitting the market to take advantage of more homebuyers and higher prices,” Watts said.

But will it be enough to fill the demand?

“That’s been a long-term challenge for real estate across Indiana,” Watts said, “but especially in the Indy area.”

Chris Dykes, managing broker for the Carmel office of Carpenter Realtors, said many buyers expected interest rates to fall this spring more than they actually will. But he’s not sure that will depress the market.

“People need a place to live, and there are a lot of folks who will make a move regardless of what the interest rates are doing,” Dykes said. “If they have the resources, they will purchase even in a market with tight inventory where they have to compete for the house they want to buy.”

Which means that, just as things have been for several years, this summer will be a seller’s market.

“There are over 75 million millennials who are in what we call the household formation phase who need a place to live and form their families,” Dykes said. “And we haven’t been able to build enough inventory in the past decade, ever since the housing crisis, to keep up with demand. That demand will continue for the next five to 10 years.”

Coastal sticker shock

Of course, things could be worse. They’re certainly much more problematic in many East and West Coast markets, where average home costs have all but priced first-time buyers out of the market. According to real estate marketplace company Zillow, the average median sales price for a home is $324,967 nationally. In the New York City area, it’s $406,667, and in Los Angeles, it’s $937,833. And yet, well-heeled buyers are still grabbing houses.

“Despite February’s supply increase, competition remains stout for attractive, well-priced listings,” Zillow stated in its February market report. “Homes that sold in February did so in 17 days—that’s slower than during the rate-fueled frenzy of 2021 and 2022 but far faster than pre-pandemic.”

Happily, things are better for Indy-area buyers, where that $285,000 median home price is far below both the national average.

“I think we’re a very attractive destination for people who live in states where the average sale price is much higher than ours,” Dykes said. “Even though we’ve experienced incredible appreciation in the last five to 10 years, sometimes in the realm of 20% per year, we still remain an affordable housing market compared with the rest of the country.”

Watts concurred, adding that the Indiana market is also fairly stable, with fewer precipitous ups and downs. For instance, while sales dropped 18% nationally last year, the Indianapolis area saw a 14% drop.

“I would say that’s much more manageable, though it’s certainly naïve to say that rate increases aren’t an issue,” Watts said. “It’s still adding $200 or $300 a month [to a mortgage payment] when you think about where we were pre-2022, versus today. So it’s still putting pressure on affordability, and we acknowledge that, but it’s perhaps not nearly as critical as it is in some other areas.”

Tough for first-timers

Paauwe, who’s made home selling and buying something of a hobby, doesn’t want to come across as a privileged boomer, talking lackadaisically about high interest rates. Today’s first-time buyers might be saddled with student debt, scrambling to pull together the cash for a down payment and paying a much higher price for prospective homes that create a truly onerous mortgage payment. For her part, she paid just $13,000 for her first home. That’s not the down payment, but the entire price.

“I have a lot of empathy for young kids who are trying to make first-time home purchases,” she said. “They’re paying rents that are just through the roof right now, so it’s hard for them to save for a down payment. And you have to make a lot more money to buy a house than you did even five, six or seven years ago. I’m at a stage in life where that’s not so much of an issue for me, but I’m not a twentysomething, who would find it much more challenging.”

Right now, selling homes has become slightly more challenging for Paauwe than it was in 2021, when she hit the market with a Carmel house in the midst of a red-hot market. It was like throwing a piece of bread into a koi pond.

“We had 56 showings that weekend, but we accepted an offer by Saturday night because it was so outstanding,” she said.

Things went more slowly—but only a little—last month when she marketed a 1,100-square-foot Fishers home on the Nickel Plate Trail. The home pulled 32 showings on its first weekend and sold for 110% of the asking price.

The fact that properties are still selling well—though not quite as well as when interest rates were low—doesn’t surprise F.C. Tucker real estate broker Matt McLaughlin. While the Washington Township area and Carmel are performing particularly strongly, he said the entire Indy-area seller’s market is still in good shape. With comparatively so few houses available, how could it not be?

“We’re still in a situation where we don’t have enough supply,” McLaughlin said. “We’re still going to see multiple offers, perhaps even above-list offers, for properties. But whereas two years ago, you might have had 10 offers on a property, we’re probably going to see two or three. It’s still going to happen, but not with that frenzied craziness we had before.”•

Please enable JavaScript to view this content.

Editor's note: You can comment on IBJ stories by signing in to your IBJ account. If you have not registered, please sign up for a free account now. Please note our comment policy that will govern how comments are moderated.