Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

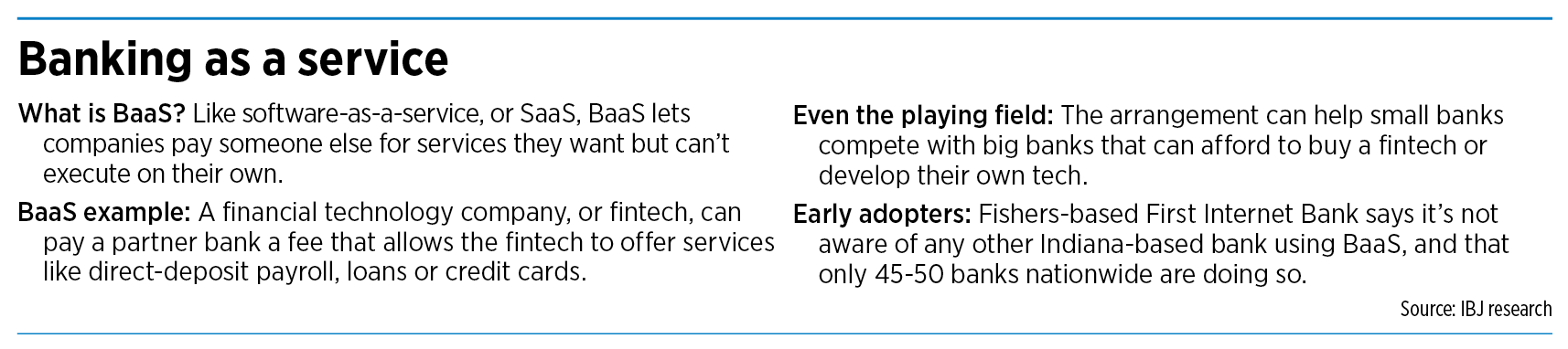

The rise in financial technology companies means it’s increasingly possible for consumers to take out a loan, transfer money or conduct other financial transactions without using a bank.

That can be bad news for those banks—but Fishers-based First Internet Bank sees an opportunity.

First Internet is among a relatively small number of U.S. banks seeking to do business with financial technology companies—fintechs—using an emerging business model called banking as a service, or BaaS.

Under this model, a bank offers its expertise and capabilities to a fintech for a fee. This allows the fintech to provide its clients services that require the involvement of a federally regulated and insured institution.

“Banking is really being revolutionized by fintechs’ entrance,” said Nicole Lorch, First Internet’s president and chief operating officer. “It’s vital for our very survival going forward to be part of a growing movement like this.”

First Internet has been involved with BaaS to a limited extent in the past, but now it’s seeking to expand this line of business. Last month, the bank announced it had reached an agreement with Synctera, a San Francisco-based startup that launched in 2020. Synctera will act as a matchmaker to help First Internet find suitable fintech partners.

Lorch said she knows of about 48 financial providers nationwide active in the space. Both First Internet and the Indiana Bankers Association said they’re not aware of any other Indiana-based banks currently involved.

But First Internet, and others, say the BaaS model is poised for growth, in part because the pandemic has accelerated the pace of adoption for online financial services. And the rollout of the federal Paycheck Protection Program, with its ever-changing rules and regulations, underscored the value of fintechs in helping banks quickly react to customer needs, said Mike Horrocks, vice president of product management at Carmel-based Baker Hill.

Baker Hill is a fintech that offers lending software to banks and credit unions.

These factors, among others, set up prime conditions for the BaaS business model, Horrocks said. “I think it’s a trend that’s going to pick up more and more and more.”

As fintechs become more widespread, he said, bank regulators and the federal Consumer Financial Protection Bureau are starting to scrutinize what the fintechs do and whether they should be regulated.

The fintechs don’t have the capability to comply with the onerous regulations that govern banks, Horrocks said. “These fintechs are going to have to find a partner that’s already used to the pressures and demands and how to deal with the CFPB and any other regulatory organization.”

Partner or purchase

The partnership model First Internet is pursuing is an alternative to what many of the big banks are doing, which is to acquire a fintech outright. Especially in the current market, where valuations for tech companies have skyrocketed, acquisition might be out of reach for smaller banks.

“Sometimes, [the fintechs are] just so darned expensive that it’s cost-prohibitive,” Lorch said, adding that First Internet wouldn’t rule out an acquisition if the price were right.

With assets of just over $4 billion, she said, First Internet is among the larger of the banks that have jumped into the BaaS model.

The bank is currently working to form partnerships with three different fintechs, two of which it learned about through Synctera. Lorch declined to name those firms because First Internet is still doing due diligence and hasn’t finalized the deals.

“We’re carefully pacing how we bring those partners aboard,” Lorch said.

But in a recent interview with the publication American Banker, First Internet CEO David Becker broadly described two of those three potential partners—one offers workers a way to access their pay at the end of each workday rather than waiting until payday; the other works with immigrants who have high-paying tech jobs but lack a traditional credit score.

Lorch said two of the pending fintech deals should be complete by the end of this quarter, with the third closing by the end of the second quarter.

Once those partnerships close, First Internet will charge the fintechs for the services it provides them. The bank will then share a portion of that revenue with matchmaker Synctera.

The arrangement offers a couple of benefits for First Internet, Lorch said. Not only will the bank earn non-interest income from the fees it charges the fintechs—it’s also a way for the bank to do more business while letting the fintech do the work of attracting that business.

Though Lorch said First Internet hasn’t set any firm goals about how much revenue it hopes to generate from BaaS, the bank has already seen success with a couple of previous BaaS partnerships.

In October, the bank announced a partnership with San Francisco-based ApplePie Capital, which offers a marketplace that matches franchise owners with lenders. ApplePie interacts with the lenders and borrowers and does most of the loan servicing, while First Internet does the underwriting and lending. Last year, First Internet did $85 million in lending through its ApplePie partnership, and the bank expects that number to grow to $150 million this year, Lorch said.

And in 2017, First Internet announced a partnership with San Francisco-based Lendeavor, a tech-enabled lender to dental and veterinary practices. Lendeavor, which now operates under the name Provide, was acquired by Fifth Third Bank last year and First Internet is no longer involved with the company.

Even further back than that, First Internet worked with Indianapolis-based ChaCha Search Inc., the now-defunct company founded in 2006 that offered a human-powered search engine. The people who did those searches for ChaCha could access their pay via a ChaCha-branded debit card linked to a First Internet account.

Transformation

Another bank active in BaaS is Cleveland-based KeyBank, which formed an in-house team two years ago to pursue BaaS opportunities. To date, the bank has formed about 10 fintech partnerships, said Kenneth Gavrity, KeyBank’s head of enterprise payments.

In some cases, Gavrity said, KeyBank has acquired fintechs. In others, it has invested in fintechs or has fintechs as customers—or both.

KeyBank has assets of $186.3 billion, does business in 15 states and operates 19 branches and 26 ATMs in central Indiana.

Gavrity said BaaS is a way of enabling what is known as embedded banking: allowing consumers to conduct financial transactions as part of some other app or experience. The ride-sharing app Uber was an early adopter of this concept, he said, because passengers could both hail a ride and pay for that ride within the same app.

Within five to 10 years, Gavrity predicted, the concept will become mainstream, allowing people to seamlessly do everything from pay a dental bill to receive an insurance payout. In some cases, consumers might know the name of the bank involved in the transaction. In other cases, they won’t.

“This is going to transform financial services,” Gavrity said.

Nymbus, a fintech based in Jacksonville, Florida, offers a similar view. The company, which works with banks to help improve their digital offerings, launched a BaaS service late last year to help banks pursue embedded banking opportunities.

Katherine Murrie, vice president of BaaS innovation at Nymbus, said she expects the current low level of participation in BaaS to grow significantly within 24 months.

“That’s a bet Nymbus is making on the marketplace, too,” Murrie said.

Gavrity sees so much opportunity in BaaS that he predicted plenty of business for First Internet, KeyBank and other financial institutions.

And if banks aren’t already active in this arena, he warned, they’d be wise to start building partnerships with fintechs now.

“There are going to be significant haves and have-nots in the banking space,” Gavrity said. “If you’re not [building fintech partnerships now], you’re not going to be able to catch up.”•

Please enable JavaScript to view this content.