Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

The amount of money banks earn from overdraft fees has dropped significantly since 2019—and that revenue might never rebound to pre-pandemic levels, observers say.

Early in the pandemic, widespread stay-at-home orders meant consumers weren’t spending as much money. Then, numerous rounds of federal stimulus payments gave millions of Americans an extra cushion of cash.

Both factors meant bank customers were less likely to overdraw their checking accounts and incur overdraft fees.

Even as the economy rebounds, a combination of factors—technological advances, competitive pressures and political scrutiny, among them—are leading banks away from overdraft fees as a revenue source. Instead, banks are rolling out a host of tools and products designed to help their clients avoid such fees.

Pittsburgh-based PNC Bank and Cincinnati-based Fifth Third Bank are among those in this market that have rolled out new overdraft-avoidance tools in recent months. Others, including Birmingham, Alabama-based Regions Bank, have announced plans to eliminate overdraft fees altogether on certain accounts.

“Everyone’s going down this path,” said Andy Baker, PNC Bank’s retail banking market manager for central Indiana, Missouri and Illinois. Baker lives in St. Louis but spends about half of his time in Indianapolis.

In the 1980s, Baker said, it was common for consultants to advise banks on how to maximize their revenue from overdraft fees. Now, the momentum is swinging in the opposite direction—possibly for good, he said.

Mike Ash, the Indianapolis-based market president at Fifth Third Bank, also predicted that the trend will continue to gain momentum. “In any industry, once a trend starts, if you don’t do it, you’re going to be left behind.”

According to S&P Global Market Intelligence, before the pandemic hit, U.S. banks had been reliably earning more than $2.5 billion per quarter from overdraft-related fees, hitting a high of $3.1 billion in the third quarter of 2019. That revenue plunged to $1.4 billion in the second quarter of 2020, rising to $2.3 billion in the fourth quarter.

During the second quarter of this year, overdraft revenue totaled $2 billion.

To be sure, overdraft fees aren’t where banks make most of their money. As a percentage of total revenue, overdraft fee revenue is in the “low single digits” for most banks, said S&P analyst Nathan Stovall.

But it’s also true that banks are finding it challenging to make money right now. They make most of their money by charging interest on loans, but that’s harder to do when interest rates are as low as they are now, Stovall said. “There’s no bank in the country that wants to lose revenue right now.”

Ease of technology

So why are banks starting to move beyond reliance on overdraft fees? Technology is one big reason.

The rise in digital payments, online banking and other financial technology means customers can track their account balances easily and quickly. It also means banks can roll out new tools to take advantage of these capabilities.

“The technology has allowed banks to provide as much information as clients want, in as close to real time as they can get,” Ash said.

In April, Fifth Third rolled out a checking account called Momentum, which includes an overdraft-avoidance tool called Extra Time. Customers who overdraw their account will have until midnight the following day to avoid a fee by adding money to their account.

Extra Time became available in the Indianapolis market in June.

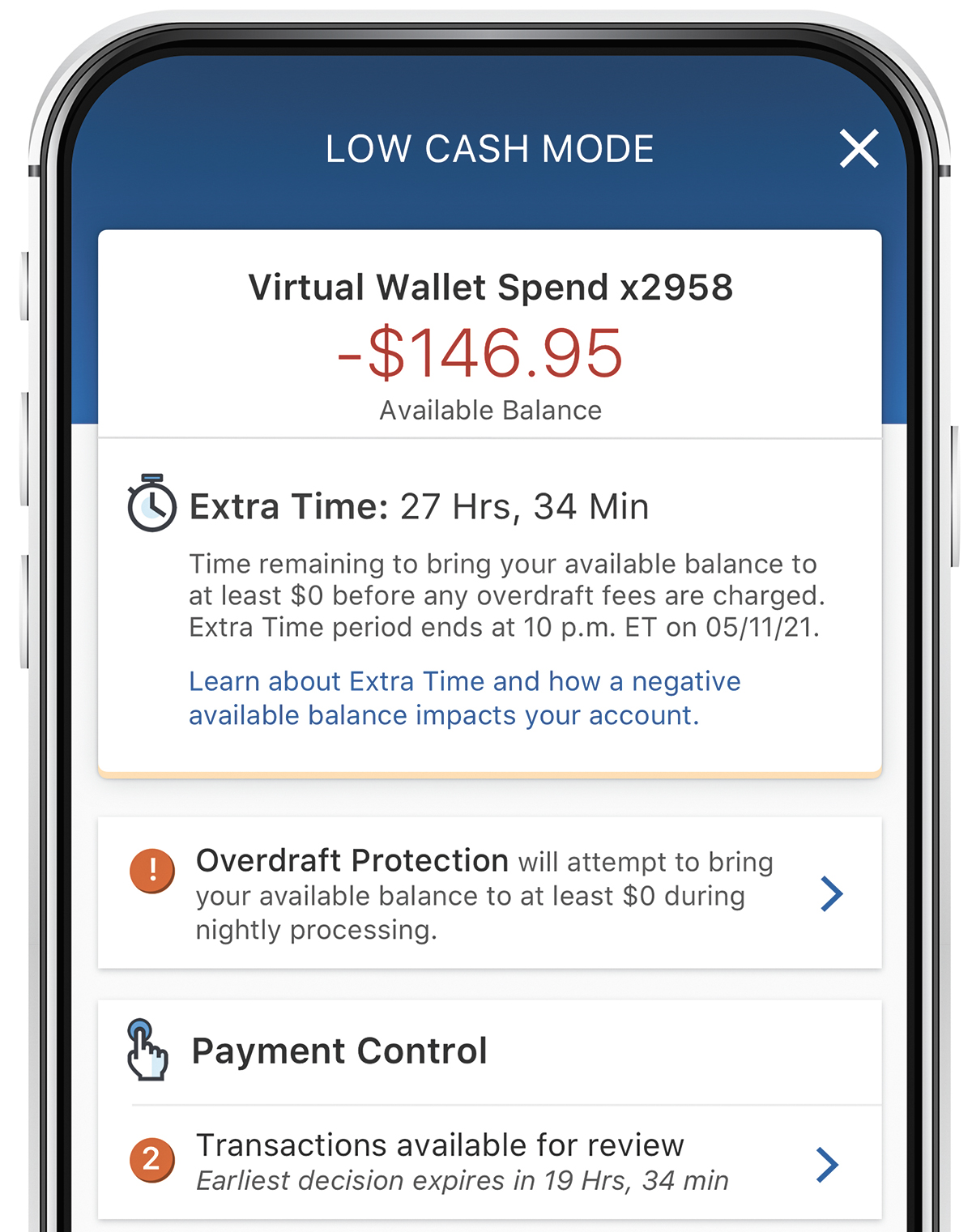

PNC’s overdraft-avoidance feature, called Low Cash Mode, debuted in April. Customers who overdraw their account receive a grace period of 24 to 48 hours to cure the overdraft by adding money to the account. If the customer is unable to do so, he or she can decide which pending withdrawals to prioritize and which, if any, to cancel.

PNC’s standard policy is to take debits from a customer’s account in the order those debits were received, Baker said. Low Cash Mode now gives customers more control over that process. “Technology is the enabler to all of this,” he said.

Since PNC introduced Low Cash Mode, the bank has already sent out more than 10 million alerts about overdrawn accounts. In about 80% of those cases, Baker said, the customer cured the overdraft within the available grace period.

PNC says it expects to see its overdraft revenue drop by $125 million to $150 million, or 50%, as a result of the change.

“There is no doubt that the short-term effect of this is dramatically less in fee revenue for us,” Baker said.

On the other hand, he said, helping clients avoid overdrafts—a major source of customer complaints—will make it easier for the bank to attract new customers and build loyalty among existing ones.

Competitors, regulators

Indeed, competition among financial institutions is a strong motivator for banks to change their ways when it comes to overdraft fees.

Online-only financial services companies such as Chime (founded in 2013), Varo Money (founded in 2015) and Dave (founded in 2017), among others, are creating new competition for banks. And that’s only heated up during the last year and a half as the pandemic accelerated the trend toward digital banking.

These companies, also known as fintechs or neobanks, have attracted a lot of investors who aren’t yet pressuring them to turn a profit—so they can afford to keep their fees minimal to attract customers.

“The investment community has given them considerable runway to really be disruptive,” Stovall said.

PNC’s Baker and Fifth Third’s Ash both acknowledged that financial technology firms are among the factors that have driven traditional banks to up their own digital games over the past several years.

“Technology absolutely has forced—in a good way—us into making the best digital products that we can,” Baker said.

Other pressures might also be in play.

Some of that pressure is coming from lawmakers and regulators, Stovall said. “You’re hearing it discussed from a lot of different places.”

In March 2020, federal regulators urged banks to waive overdraft charges and other fees in light of the pandemic. In May of this year, Sen. Elizabeth Warren, a Democrat from Massachusetts, grabbed headlines during a Senate Banking Committee meeting when she berated JP Morgan Chase Chairman and CEO Jamie Dimon for the bank’s pandemic overdraft practices.

In November, Regions Bank disclosed that it was under investigation by the Consumer Financial Protection Bureau for its overdraft policies and practices. The investigation remains ongoing.

The CFPB also fined Regions $7.5 million in 2015, saying the bank had charged customers for overdraft coverage services for which the customers had not agreed to opt in, in violation of federal law. Regions reimbursed customers more than $49 million as part of that 2015 action.

Regions, which operates 25 branches in the Indianapolis area, plans to launch a checking account by the end of this month that will charge a monthly fee, but no overdraft fees. The bank has also made other changes, including lowering its maximum daily overdraft fees and enhancing the account alerts it sends to customers.

In a call with analysts in July, Regions CFO David Turner Jr. said the bank expects its overdraft fee revenue to decline 10% to 15% from pre-pandemic levels because of these changes.

In court

Litigation might also play a role in making overdraft fees less attractive, said Lynn Toops, a partner at Indianapolis-based law firm Cohen and Malad LLP. “There is a ton of litigation over overdraft fees, and so it could be a reaction to that.”

Cohen and Malad started suing banks over their overdraft practices within the past five years, Toops said, after some earlier court decisions convinced the firm this was an area of opportunity.

Since then, she said, her firm has litigated “probably hundreds” of such cases around the country and has achieved dozens of class-action settlements that recovered tens of millions of dollars for bank customers.

“We’ve won a lot more than we’ve lost,” Toops said.

Her victories include a case against Cincinnati-based First Financial Bancorp that was filed in U.S. District Court in the Southern District of Indiana. First Financial settled that case last quarter for $3.8 million, the bank disclosed in a financial filing.

Toops’ pending overdraft-fee cases include one filed in June in Delaware County against Muncie-based First Merchants Bank and one filed in July 2020 in Marion County against Jasper-based German American Bank. The parties in the German American case are attempting to resolve that dispute through mediation.

In all three of these cases, Toops is using a breach-of-contract argument. The cases allege, among other things, that the banks are assessing overdraft fees in a way that violates terms and conditions customers had agreed to.•

Please enable JavaScript to view this content.

Editor's note: You can comment on IBJ stories by signing in to your IBJ account. If you have not registered, please sign up for a free account now. Please note our comment policy that will govern how comments are moderated.