Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

For a 26-year-old medical practice with big growth plans, Urology of Indiana felt it needed to make a move.

The specialty practice—with clinics in Carmel, Fishers, Avon, Greenwood and other cities around central Indiana—wanted to expand statewide and compete against other urology practices, many owned by large hospital systems. But it felt it needed a bigger partner, with deeper pockets, to help it make the leap.

So after 18 months of exploring options, the practice announced in January it agreed to be acquired by suburban Nashville, Tennessee-based U.S. Urology Partners, a large national practice backed by private-equity firm NMS Capital, based in New York City, with $1.5 billion in assets under management.

Now, with the money its partner can provide, Urology of Indiana is mapping out its future.

“We’re going to be expanding into new markets—Bloomington and Kokomo to start with others to follow,” CEO Britt Moster said. “And then we’ll just continue to develop our service lines, bring new technologies, new therapies to the market.”

It’s a pivotal moment for Urology of Indiana, formed in 1997 but with roots under various names back to 1887, when Dr. William Wishard founded Indiana University School of Medicine’s urology department.

The practice is far from alone in turning to private equity. Physician practices statewide and around the nation are being purchased by groups that invest capital in private companies, often taking ownership control and seeking to increase their profitability.

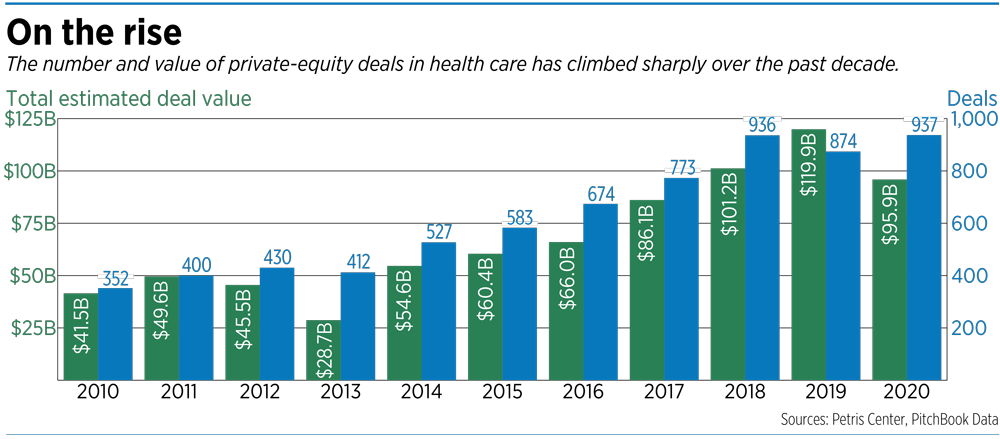

The number of acquisitions by private-equity firms in the United States has soared from 75 deals in 2012 to 484 in 2021, a more-than-sixfold increase. That’s according to a study released in July by the American Antitrust Institute, the Petris Center on Health Care Markets and Consumer Welfare, the University of California at Berkeley, and the Washington Center for Equitable Growth.

Private-equity firms, which pool money from wealthy individuals and institutional investors, typically offer physician practices a combination of immediate cash and shares of their existing business to the owners.

They often do it by creating a large “platform” practice in that specialty, then acquiring smaller practices in the specialty, potentially creating economies of scale and increasing bargaining power with insurance companies.

The large private-equity firms say the deals benefit patients and physicians alike, helping the practices to become stronger and more competitive with new technology and facilities.

But some others warn that the spiraling number of deals could lead to some large physician groups having an unfairly high market share, which could lead to price increases and cost-cutting.

“Cutting costs often involves cutting workers or replacing highly paid [and highly qualified] workers with lower paid [and less highly qualified] workers,” the American Antitrust Institute study found. “It might also involve switching to cheaper supplies, such as sutures and tubing, or reducing hours or [closing] entire facilities.”

Impact of private equity

Where a single private-equity firm gained control of more than 30% of the market, prices to patients for care increased as high as 13% in dermatology, 16% in obstetrics and gynecology, and 18% for gastroenterology, the study added.

Another study, published in July in the British Medical Journal, found that private-equity investment was associated with up to a 32% increase in costs for payers and patients.

And recently, federal regulators have taken more notice of private-equity deals. In September, the Federal Trade Commission sued medical group U.S. Anesthesia Partners, based in Dallas, and its private-equity backer, Welsh Carson Anderson & Stowe, accusing them of scheming for more than a decade to acquire anesthesia practices in Texas, eliminate competition, hike prices and increase profits.

“This conduct has resulted in egregious price increases for patients and their employers, on the order of tens of millions of dollars or more each year,” the FTC complaint said.

U.S. Anesthesia Partners has 4,500 clinicians serving 2 million patients in nine states (none in Indiana). A spokesman for the company said the FTC action “threatens to disrupt and restrict patients’ equitable access to quality anesthesia care in Texas and will negatively impact the Texas hospitals and health systems that provide care in underserved communities.”

The FTC oversees mergers and acquisitions to ensure they do not result in monopolies. It typically focuses on buyouts of more than $100 million.

But FTC Chair Lina Khan said in remarks to the American College of Emergency Physicians last month that she wants to change that so the agency is “made aware of private equity acquisitions that may fall under the $100 million threshold.”

In the meantime, the pace of acquisitions by private-equity firms shows no sign of slowing.

Within the past 12 months, three Indiana orthopedic physician groups—Indianapolis-based Midwest Center for Joint Replacement, Muncie-based Central Indiana Orthopedics and South Bend Orthopedics—have all been acquired by OrthoAlliance, a large practice based in Cincinnati and backed by Revelstoke Capital Partners of Denver.

In announcing the various deals, the two sides touted the benefits to patients. Central Indiana Orthopedics—founded in 1950 and now with 26 physicians and clinics in Fishers, Anderson and Muncie—said its patients will see no changes in their doctors or services.

“Instead, they will benefit from greater access to the latest surgical and medical advances as well as additional resources and investment as the partnership flourishes,” Dr. Jamie Kay, president of Central Indiana Orthopedics, said in written remarks when the deal was announced in November 2022.

Yet, some larger orthopedic practices say they are rebuffing private-equity deals because they don’t want to lose their independence and take direction on such things as services, prices, employee work conditions and patient-physician face time.

Fielding the pitch

John Ryan, CEO of OrthoIndy, a physician-owned practice and hospital based on the northwest side with more than 100 doctors, said he gets at least two calls a week from private-equity firms, pitching him on an acquisition.

The typical pitch, he said, is that the large private-equity firm will buy a piece of the practice—sometimes just the administrative back office—and will let OrthoIndy retain some ownership.

The upside is an initial inflow of capital and the promise of a bright future with a big partner. The downside is the possibility of restructuring operations, adding debt and even lower physicians’ compensation.

His answer: not interested.

“It’s really not worth the loss of control that you’ll have over your own destiny,” he said.

Dr. Ed Hellman, an orthopedic surgeon and chair of the OrthoIndy board, said the firm hired bankers several years ago to help it market the practice to potential buyers in private equity “to see what kind of offers were out there.”

“We probably spent about a year going through this process, and at the end, we came to the conclusion that there really wasn’t much we thought they would bring to the table other than the obvious big check at the beginning,” Hellman said.

He declined to say what kind of offers the OrthoIndy board received. But across the board, all the private-equity firms promised to stay out of clinical decision-making and let physicians continue to treat patients as they saw fit.

“We were a little skeptical about how successfully they would stay out of it,” Hellman said. “In other words, if they’re cutting back on the resources that we have available to us, that’s going to eventually affect the care you can provide.”

Some financial experts say the economics of private-equity deals in health care can squeeze small practices, and by extension, patients.

That’s because many private-equity firms hold on to small practices for a relatively short time, usually four to six years, before selling them to another investment group. So they want to quickly make the small practice more profitable and thus attractive to the next buyer, reaping a quick profit for themselves.

“If I think about putting the patient at the center of the universe, I don’t think the end game should be the profit I can generate by flipping a practice,” said Mike McCaslin, an accountant with CBIZ Somerset in Indianapolis.

Some small and medium-size physicians’ practices say they are not interested in partnering with private equity and are determined to stay independent.

Cancer Care Group, an Indianapolis-based practice of about 20 radiation oncologists, has not considered or initiated any offers from private equity, “but I get my share of emails soliciting opportunities,” CEO Steve Freeland said.

“I hear very mixed messages on the overall satisfaction [and] success of these deals after the fact,” he added. “None of what I hear would compel Cancer Care Group to consider this option.”

And sometimes staying independent means having to compete against larger players that have taken private-equity money.

Northwest Radiology Network, an Indianapolis-based group of about 30 radiologists, was replaced last year as the dedicated radiology group for Ascension St. Vincent’s hospitals in central Indiana. The new contractor was Radiology Partners Inc., a national group based in suburban Los Angeles, backed by private-equity firm Whistler Capital.

Radiology Partners, formed 10 years ago, has been growing quickly and bills itself as the largest radiology practice in the United States, serving more than 3,250 hospitals and other health care facilities.

But the torrid pace of growth seems to have come with a price. In June, S&P Global Ratings downgraded the national practice, saying its capital structure could become unsustainable.

The group has seen more money flowing out than in the past two years, due to its “aggressive” stance on acquisitions, S&P analysts noted.

When things go wrong

Taking on too much debt can sometimes lead to bankruptcy, something that has happened several times recently.

In September, American Physician Partners, based in Brentwood, Tennessee, filed for bankruptcy and said it decided to wind down its business after efforts to negotiate with secured lenders and find a buyer failed, according to The Wall Street Journal.

The company, with 2,500 doctors and backed by Brown Brothers Harriman Capital Partners, made the move to dissolve just a few months after ending its relationships with 150 hospitals and emergency departments in 15 states. The company listed roughly $630 million in debt and up to $500 million in assets.

That was the second large bankruptcy of the year. In May, Envision Healthcare, an emergency physicians’ group based in Nashville, filed for Chapter 11 reorganization, saying it was weighed down by high labor costs and the lingering effects of the pandemic. The group, backed by private-equity giant KKR & Co., has more than 25,000 physicians and clinicians.

But if such risks bother some Indiana physician practices that have cut deals with private equity, they are not showing it.

At Urology of Indiana, officials say partnering with private equity was the best option for staying competitive in an increasingly consolidating market.

“We recognize that consolidation in health care is here, whether we want it to be or not,” said Moster, the CEO. “And we believe that the national urology platforms are the next growth iteration for us.”

The firm’s new owner, U.S. Urology Partners, said the Indiana firm will continue to make its own clinical and financial decisions. The national company has bought urology practices in Florida, New York, Ohio and Massachusetts, in addition to Indiana. It said it expects to continue buying urology practices looking for more money to grow.

“Like any growing business, you come to a point where you need some pretty significant investment to keep on the trajectory you are on,” said Corina Tracy, CEO of U.S. Urology Partners. “You need some infrastructure … you know, more equipment, more technology to really take that next step and continue to provide care.”

Both sides declined to disclose the terms of the deal, or to discuss Urology of Indiana’s finances. Moster said the practice spent more than a year examining numerous options before deciding private equity backed by U.S. Urology was the best fit.

“We didn’t need to do it,” she said. “We decided to do it because it was just the right next step for our practice.”•

Please enable JavaScript to view this content.

When will the patient be the primary driver of economic decisions when it comes to healthcare?

Is bigger always better or more profitable for healthcare systems or physician groups?

Are the latest gadgets and gizmos going to ensure better delivery of healthcare or improve healthcare outcomes?

How much personal income do these physician groups really need to have happy and productive lives?

Healthcare delivery in Indiana is in pretty sad shape now. But just wait for the carpet baggers to become more dominant in our State.

Phillip D. Toth, MD, FACP