Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe NowIndiana-based banks say they haven’t seen big loan losses so far, thanks to the various federal COVID-19 stimulus and relief programs that are helping support the U.S. economy.

However, amid the economic uncertainty—and even though some banks express reasons for optimism—they are preparing themselves now for the losses that likely lie ahead.

“I believe we have a long way to go before we will know or understand the impact of the economy being shut down,” First Merchants Corp. Chief Credit Officer John Martin told analysts during a July 23 earnings call. “The economy is presently being buoyed by stimulus that will eventually end.”

Over the past two quarters, Muncie-based First Merchants, like other Indiana-based banks, has been significantly increasing the amount it sets aside for possible loan losses. In doing so, the banks are echoing the actions of the country’s largest financial institutions, including JPMorgan Chase & Co., Fifth Third Bancorp and Bank of America Corp.

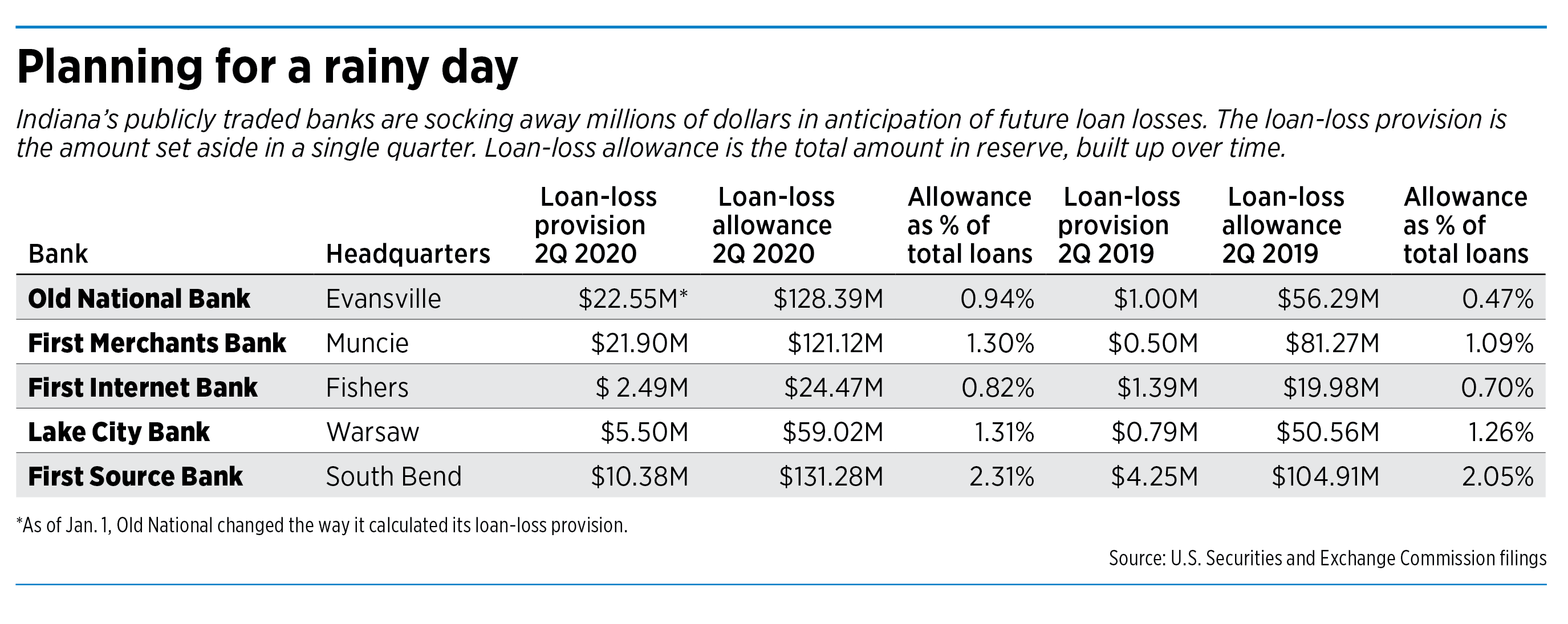

Each quarter, banks set aside a provision for loan losses—a certain amount of money to cover potential bad loans. Banks can vary the amount they set aside each quarter, based on factors such as the size of their loan portfolio, how they expect those loans to perform and how much they already have in reserve.

If a bank dramatically increases its loan loss provision, that can mean it anticipates trouble to come.

In the second quarter, First Merchants set aside a provision of $21.9 million, following a $19.8 million provision in the first quarter. In comparison, the bank set aside just $500,000 during the second quarter of 2019.

The increased provision, the bank said in its earnings release, “primarily reflects our view of increased credit risk related to the COVID-19 pandemic.”

Other Indiana-based banks have taken similar actions.

Evansville-based Old National Bancorp, the largest Indiana-based financial institution, set aside $22.6 million in the second quarter, up from $17 million in the first quarter and $1 million in the second quarter of 2019. (Part of the increase from 2019 to 2020 stemmed from a Jan. 1 change in how Old National calculates its expected loan losses.)

“Our credit-quality metrics improved during the quarter, but we expect that losses will ultimately materialize once the stimulus and deferral programs run their course,” Old National CEO Jim Ryan told analysts during a July 20 earnings call.

Warsaw-based Lakeland Financial Corp., parent of Lake City Bank, set aside $5.5 million in the second quarter—down from the $6.6 million it set aside in the first quarter but up dramatically from the $785,000 it set aside during the second quarter of 2019.

Fishers-based First Internet Bancorp set aside $2.5 million last quarter, up from $1.5 million in the first quarter and $1.4 million in the second quarter of 2019.

Even so, First Internet CEO David Becker told IBJ he sees reasons for optimism. “Knock on wood, we think we’re really in pretty solid shape.”

One encouraging factor, Becker said, is that fewer of the bank’s loans are on deferral than were a few months ago.

As of mid-May, $633.6 million in loans—22% of the bank’s loan portfolio—was on deferral. Becker said many of those deferrals went to dental practices whose source of income dried up when they were forced to temporarily close their offices to all but emergency cases during the shutdown.

By June 19, deferrals had dropped to 18.6% of the bank’s portfolio. And by July 17—early in the third quarter—deferrals made up only 12.6% of the bank’s portfolio. Since July 1, the bank has granted only a handful of new deferrals, Becker said, and all borrowers who have exited deferral have resumed making regular payments.

At the end of the quarter, First Merchants had $1.1 billion in loans, or 12.1% of its loan portfolio, under some sort of modification. Commercial real estate loans, which make up about a quarter of the bank’s portfolio, were the category most likely to be granted modifications: 29.1% of loans for owner-occupied commercial real estate had modifications, in addition to 25.9% of loans for non-owner-occupied commercial real estate.

As of June, 11% of Old National’s loan portfolio, or $1.3 billion, was under deferral. That includes 14% of the bank’s commercial loans and 3% of consumer loans and mortgage loans.

At Lake City Bank, $653 million, or 15% of the bank’s loan portfolio, was under deferral as of June 30. By July 22, that had dropped to $425 million in loans, or 9% of the total portfolio.

Federal regulators in late April gave banks the leeway to grant deferrals rather than play hardball and push loans into default.

Under the policy announced at that time, lenders could grant deferrals for up to six months without having to categorize the loans as past due if the borrowers had been otherwise current on payments.

The deferrals have helped prop up banks’ loan portfolios amid the economic downturn, said Nathan Stovall, lead banking analyst at S&P Global Market Intelligence. “No doubt it has masked what would probably be a pretty big spike in problem loans.”

The deferrals won’t be enough to save all those loans from going bad, Stovall said.

According to S&P’s analysis, “broadly speaking, we assume that 30% of loans that were deferred will eventually end up in nonaccrual,” Stovall said. “They deferred for a reason. There was a problem there or some stress there.”

Another factor keeping loan defaults in check right now: the various forms of federal COVID-19 relief, including Payroll Protection Program small-business loans, enhanced unemployment benefits and individual stimulus payments.

Congress has been debating possible additional relief measures, and starting Aug. 10, PPP borrowers can begin submitting documentation to see if they qualify for total or partial loan forgiveness.

Once stimulus measures run their course, Stovall said, banks will have a better idea of what kind of loan losses they’re facing. “The proof will really come late this year or maybe even next year,” he said.

Stovall predicted that loan losses will peak in 2021, though this is based on some key assumptions: that a COVID-19 vaccine is available next year, and that the economy has revived by then. “If that didn’t happen, things would look quite a bit different.”•

Please enable JavaScript to view this content.

Editor's note: You can comment on IBJ stories by signing in to your IBJ account. If you have not registered, please sign up for a free account now. Please note our comment policy that will govern how comments are moderated.