Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

When activist investor Paul Singer sets his eyes on a struggling company, he makes waves.

The billionaire acquired bookstore chain Barnes & Noble, which had suffered seven years of declining revenue, for $683 million in 2019 and installed a new CEO who fired nearly half of the company’s New York-based book buyers and allowed store managers to decide which books to buy.

Singer took a $3.2 billion stake in telecom giant AT&T and called for sweeping changes in the underperforming company. Less than a year later, the chief executive stepped down and his successor announced plans to undo a huge acquisition by spinning off WarnerMedia.

Singer scooped up 9.2% of the shares in Athenahealth, a company that digitizes patient medical records and billing claims for hospitals. In response, the company announced plans to close offices, lay off hundreds of people and sell one of its two corporate jets. Unsatisfied, Singer pushed out the company’s co-founder and CEO, Jonathan Bush, cousin of former President George W. Bush, and installed a replacement.

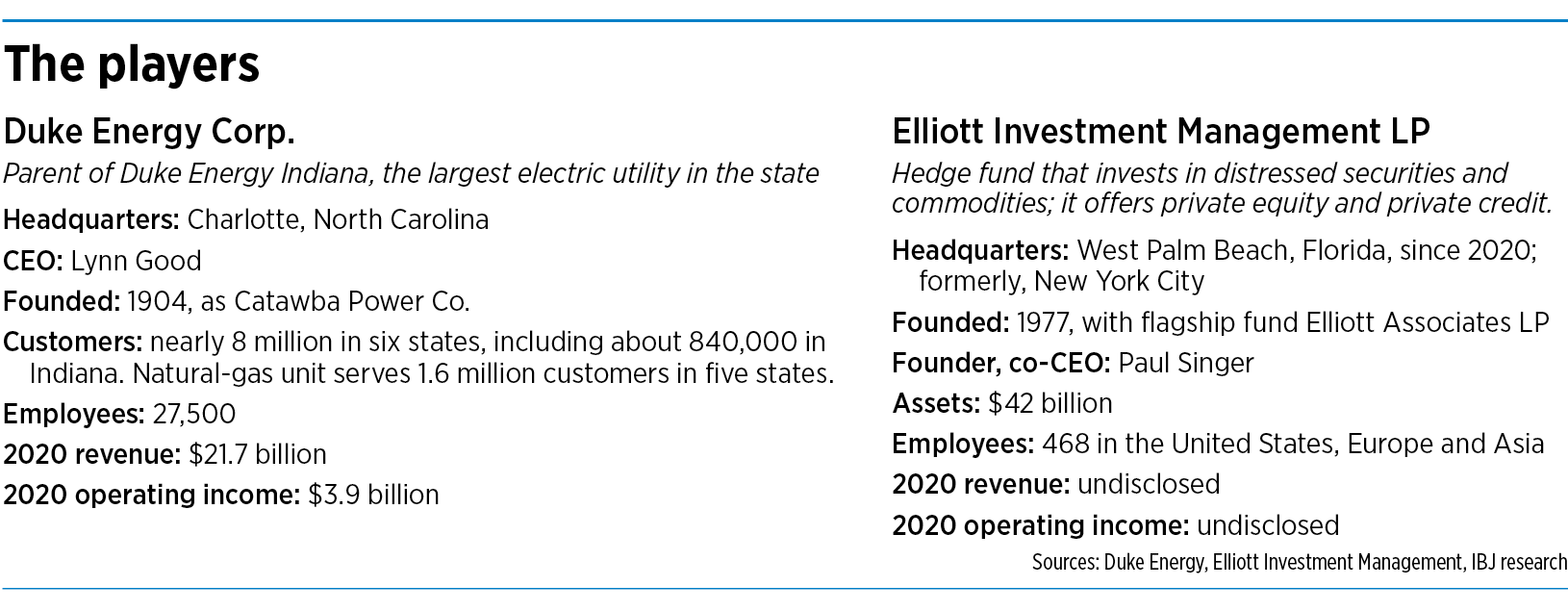

Now, Singer is rocking the boat again, this time with his sights set on Duke Energy Corp., the North Carolina-based parent of Duke Energy Indiana, the state’s largest electric utility.

The question is whether Singer will again be successful in getting his demands met, even if it means turning the utility on its head.

Singer’s hedge fund, Elliott Investment Management LP, last month sent a letter to Duke Energy, urging it to consider separating into three companies. The letter said the huge utility has been underperforming its peers and argued that Duke’s customers would be better served by locally managed utilities.

Singer’s vision: He wants the companies split along geographic lines, with one covering the Carolinas; another covering Florida; and the third covering Indiana, Ohio and Kentucky. Elliott’s letter said the split would unlock up to $15 billion for shareholders. Elliott is also asking for three seats on Duke’s board, saying the company needs new direction.

The letter said Elliott was one of Duke’s 10 largest shareholders, following large purchases of stock. It did not reveal what percentage of Duke stock it holds today.

“Despite a portfolio of top-tier utilities, Duke has suffered numerous operational setbacks and investment and strategic missteps over the past decade, at significant cost to both shareholders and customers,” Elliott wrote to Duke’s board on May 17. It publicly released the 15-page letter the same day.

Breakup after buildup?

In response, Duke said it would review Elliott’s proposals, but countered that breaking up the company would be a mistake, “as scale is needed to efficiently finance the company’s unprecedented capital investment and growth opportunities.” It added that the proposed breakup posed capital structure and credit problems.

Duke said Elliott’s push is just the latest in a series of proposals the hedge fund has offered the utility since last summer.

“Throughout, Duke Energy’s board of directors has reviewed their proposals in depth and determined that they are not in the best interests of the company, its shareholders and other stakeholders,” Duke wrote in a five-page response.

The power struggle comes just four months after Duke announced plans to sell nearly one-fifth of the Indiana operation to the government of Singapore for $2.05 billion. The company said the deal, which is littered with redacted documents and non-disclosure agreements, will help it raise money to fund its clean-energy transition and fund other initiatives.

But consumer and environmental groups question whether the deal is likely to benefit Indiana customers and are raising sharp questions about the secrecy.

The twin announcements thrust Duke into the spotlight and raise questions about whether Duke is on the right course in a challenging environment for utilities or is getting unnecessarily sidetracked.

A corporate breakup, undoubtedly an extreme move, would undo years of corporate building at Duke Energy, a running project largely carried out by former Duke CEO Jim Rogers. Over 30 years, starting in 1988, Rogers built Duke into the nation’s largest electric utility through a series of mergers that began in Indiana with a nearly insolvent utility called PSI Energy.

Rogers retired in 2013 as CEO after 25 years with the company and its predecessors. He died in 2018 at the age of 71.

Today, Duke provides electricity to nearly 8 million customers in six states, including 840,000 in Indiana.

Company setbacks

The company, however, has faced expensive setbacks in recent months. In January, it agreed to absorb $1.1 billion in costs, rather than have customers pick up the cost, for getting rid of hazardous coal ash stored near one of its large generating plants in North Carolina following a huge spill into the Dan River.

In another expensive move, Duke and a partner, Dominion Energy, announced last summer they had canceled an $8 billion pipeline project that would have carried natural gas across the Appalachian Trail, as costs rose and environmental groups sued to block the project. That resulted in a $1.6 billion write-off for Duke.

In March, Moody’s downgraded its rating on Duke’s long-term debt, citing the recent settlement of coal-ash cleanup.

Singer’s hedge fund, Elliott, cited all of those setbacks in its letter to Duke’s board, and urged the company to take huge steps to restructure.

“Under the current structure, Duke has been unable to execute effectively and maximize the potential of its premium utility franchises,” Elliott wrote in the letter, signed by two senior managers.

Elliott officials declined further comment on the record to IBJ.

Duke Energy said its Indiana operations are well managed and a breakup would not help.

“We have become a strong, better company through mergers over the years while keeping our deep, local roots in the state,” the company said in an email to IBJ. “Our charitable community giving has increased, our economic development work is robust, and we still have local managers who serve on boards and live in the communities we serve. As a Wall Street activist hedge fund, Elliott Management does not have any of the same ties and commitments.”

The company forwarded several reports from analysts who are critical of splitting up the company and suggested that Indiana House Speaker Todd Huston might have some thoughts on this issue.

IBJ reached out to Huston’s office and a few days later he issued a statement.

“We are monitoring the buyout discussions around Duke Energy as it relates to Indiana, and share concerns about the possibility of unintended consequences, including significant ratepayer increases and modernization stagnation,” Huston said in the written statement. “Duke Energy Indiana, our state’s largest utility, continues to be a great community partner as we continue to grow economic development throughout the state, and I hope we can avoid any significant disruptions.”

Activist investor

There’s no question that Singer, who created the Elliott hedge fund in 1977 (Elliott is his middle name), will push Duke hard for an overhaul. He is not the type of investor who buys stock in a company, then patiently waits for management to deliver results.

Instead, Singer has built a reputation as an agitator who uses his $42 billion fund to buy stock in companies he deems weak. Then he pressures management to make huge changes, with the goal of improving the stock price.

“A signature Elliott tactic is the release of a letter harshly criticizing the target company’s CEO, which is often followed by the executive’s resignation or the sale of the company,” wrote The New Yorker in a 2018 profile of Singer.

Bloomberg called Singer “aggressive, tenacious and litigious to a fault,” and dubbed him “the world’s most feared investor.” Fortune magazine described him as one of the “smartest and toughest money managers” in the hedge fund industry.

But some critics say activist investors like Singer don’t build companies but instead push hard for layoffs, divestitures and a cutback in new investment to make a company more profitable, often just in the short term.

The former president of Argentina, Cristina Fernández de Kirchner, once described Singer as a “bloodsucker” and a “financial terrorist” after the country defaulted on $80 billion of debt in 2001 and the country offered creditors 30% of what they were owed. Many took the deal, but Singer and a few other hedge funds refused to go along, pushing for full repayment.

Singer, for his part, has argued that activist investors like him can shake up mismanaged or dysfunctional organizations, whether they be underperforming companies or countries defaulting on bonds.

He wrote in The Wall Street Journal in 2017 that many activists are interested in the long-term value of a company, and too often, companies hide behind “long term” as a way to justify prolonged underperformance.

“Equity activism means using your voice and voting rights to improve companies in ways that maximize value for all shareholders,” he wrote under the headline “Efficient Markets Need Guys Like Me.”

Not always the winner

Singer doesn’t always get his way. His scorecard has a few losses or incompletes when target companies fight back.

In 2011, for example, Elliott sued Vietnamese state shipbuilder Vinashin in British High Court to recover its investment in a $600 million syndicated loan that Vinashin defaulted on a year earlier. Vinashin had initially offered repayment of 35 cents on the dollar to bondholders before Elliott filed the suit, according to The Wall Street Journal. Elliott sued for full repayment, with unpaid interest, totaling $13.2 million. A year later, however, Elliott quietly dropped the suit.

In 2017, Elliott tried to force Akzo Nobel, the Dutch paint and chemicals company, to oust Chairman Antony Burgmans and to sell itself to American rival PPG Industries. But after months of court fights, the two sides announced a truce, with Akzo Nobel remaining independent.

Singer is estimated by Forbes to have a personal net worth of $4.3 billion. Last year, the magazine ranked him 222nd on the list of the 400 richest Americans.

What caused him to take an interest in Duke Energy remains unclear. But the utility has been popping up in the news lately as something of a problem child, with the expensive cancellation of its Appalachian pipeline, the costly settlement over its coal-ash ponds and other issues.

In September, The Wall Street Journal reported that NextEra Energy, a smaller utility based near West Palm Beach, Florida, whose largest operating company is Florida Power & Light, made a takeover approach to Duke, in a move that would create a $60 billion combination. Duke rebuffed the offer, the newspaper reported.

In its letter to the Duke board, Elliott said it has followed Duke and the U.S. utility industry for almost 20 years.

It said the company’s operations in Indiana, Florida and some other states were once operated as separate, stand-alone companies, “each having more-than-sufficient scale to operate successfully and thrive.”

Road to Duke Energy

Elliott’s reference to local corporate history is likely to hit home for Indiana. In 1988, Rogers, a lawyer and former journalist, took over a small, struggling utility then called Public Service Company of Indiana.

The company was nearly bankrupt after spending more than $2 billion in a failed attempt to build a nuclear power plant in Marble Hill, a small Indiana town on the Ohio River. Costs for the plant had spiraled out of control and PSI was running out of money. PSI abandoned the project and auctioned it off for parts in 1985.

Rogers worked to rebuild PSI, and fought off a takeover attempt by the much larger IPALCO, parent company of the Indianapolis electric utility now called AES Indiana.

Rogers then engineered a merger with Cincinnati Gas & Electric Co. Even though PSI was the smaller partner, Rogers became vice chairman and chief operating officer of the combined companies, called Cinergy Corp., and later rose to CEO.

Four years later, he pulled off another merger, this one with Duke Energy, and again wound up as CEO.

In 2011, Rogers pulled off perhaps his most significant deal, the $13.7. billion acquisition of Progress Energy, based in Raleigh, North Carolina. That deal made Duke the nation’s largest electric utility, a title previously held by Southern Co., based in Atlanta.

But as far as Elliott is concerned, bigger is not better in Duke’s case. It said that a separation of the company into three smaller companies would create $12 billion to $15 billion of near-term value for shareholders, based on the metrics of Duke’s closest peers.

It estimated that the Carolinas, Florida and the Midwest (comprising Indiana, Ohio and Kentucky) would command equity market valuations of $55 billion, $23 billion and $15 billion, respectively, for a total equivalent of $93 billion.

That’s $16 billion above the $76.9 billion in market value Duke now commands, based on its closing price of $100.08 on June 1.

Skeptics

Yet some analysts are not convinced that Elliott’s prescription is the right medicine for Duke or that the stock would be more valuable after a breakup.

“Color us skeptical that separating Duke into smaller utilities would prompt a near-term re-rating in Duke’s share price,” wrote Wells Fargo analyst Neil Kalton in a May 17 note to clients.

He said he agreed with Duke management that a “shrink-the-company” strategy would require significant costs for each of the three companies to set up corporate functions, and that investors would not automatically respond by driving up the share prices of three companies.

Morgan Stanley analyst Stephen Byrd said he doubts the Duke board and Elliott will reach agreement on any element of Elliott’s proposal, or that Duke will materially alter its strategy. “The cost of refinancing debt and establishing separate capital structure for 3 separate entities could be significant,” he wrote.

Indeed, shareholders seem to have responded mostly with a big yawn. Duke’s stock, which closed at $103.06 the day before Elliott released its letter, rose briefly as high as $108, but has since fallen back to the $100 level.

Nor do some consumer groups seem sold on the idea of a breakup, although they say local control is often better.

Tyson Slocum, energy director at Public Citizen, the not-for-profit consumer group founded by Ralph Nader, said that, while breaking up Duke could have benefits, such a move should be made through careful deliberation involving employees, customers and communities.

“Elliott is not an agent of positive change for Duke,” he wrote in an email to IBJ. “It is a vulture hedge fund with a decades-long track record of disruptive and destructive behavior.”

Citizens Action Coalition of Indiana, a grassroots consumer organization, said it accepted the premise that Duke is too big, and utilities should be managed and operated as close to the communities they serve as possible.

“Our local public utilities should not be fodder for massive energy holding companies or for hedge funds to do with as they please,” Kerwin Olson, CAC’s executive director, wrote in an email to IBJ. “Neither of those entities have the best interest of consumers or the communities they serve in mind.”•

Please enable JavaScript to view this content.

Good article. I am puzzled why Duke would suggest Speaker Huston would have comments on a potential break up rather than IURC or OUCC.