Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

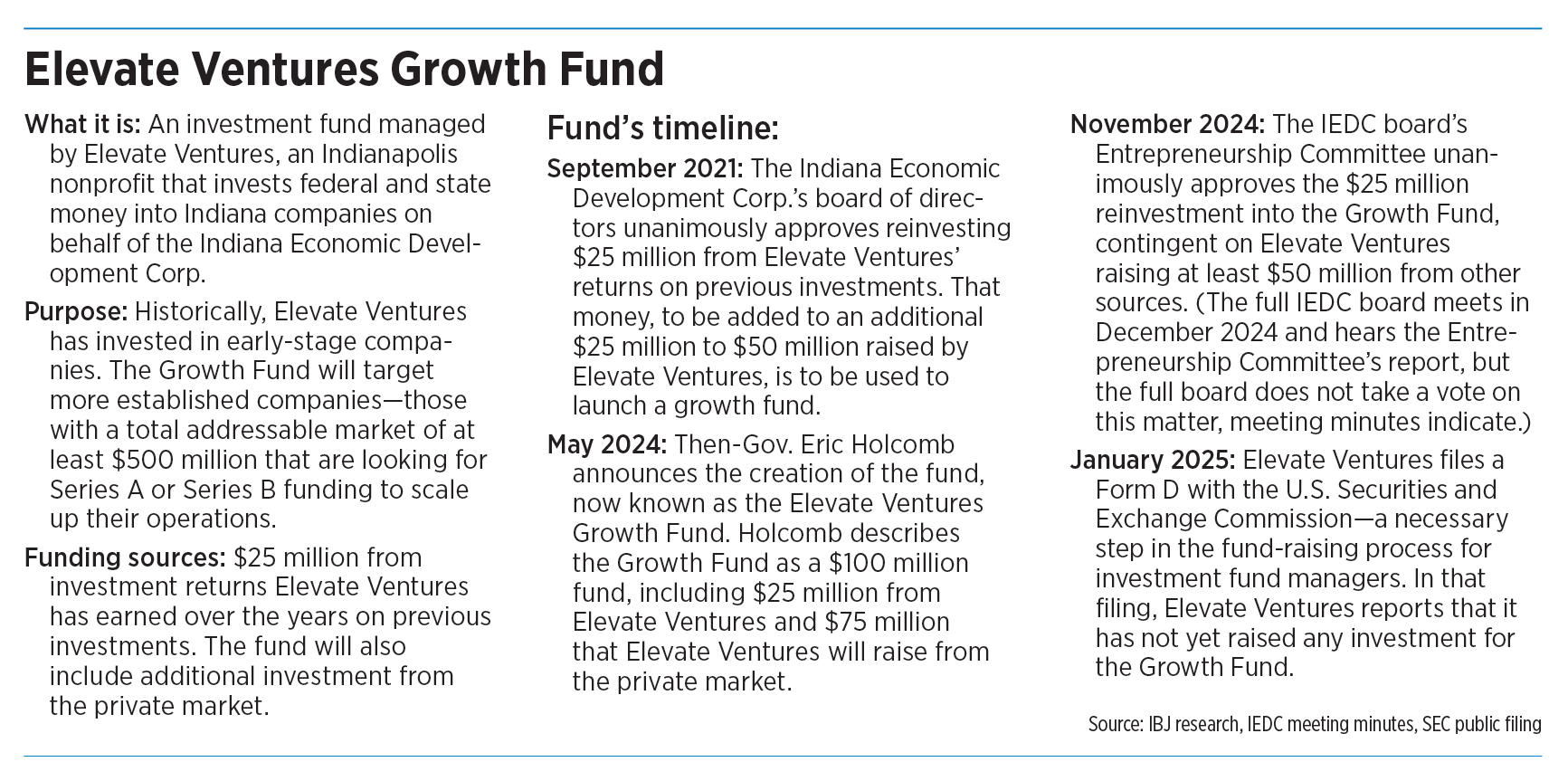

Almost exactly one year ago, Indiana officials publicly announced a significant entrepreneurial resource the state had been quietly working on for several years—the launch of a $100 million investment fund to help young companies scale up their businesses.

The fund, known as the Elevate Ventures Growth Fund, would be managed by Elevate Ventures, an Indianapolis-based nonprofit that invests federal and state money into companies on behalf of the Indiana Economic Development Corp.

The new fund would differ in important ways from Elevate’s other investment funds: Namely, it would be primarily made up of money from the private market.

It also would enable larger investments into later-stage companies than Elevate has targeted since its 2011 launch. And the Growth Fund’s fee structure would be different from Elevate’s other investment funds. The state wouldn’t pay Elevate an upfront cost to manage the fund; instead, it would operate more like a traditional investment fund with fees and a percentage cut of the returns if its investments did well.

But a lot has changed since the state’s announcement last May.

Most notably: A new gubernatorial administration is in place—and has expressed skepticism about past IEDC activities and decisions. Gov. Mike Braun has frozen funding earmarked for Elevate Ventures, with little explanation about why or how the move will impact the nonprofit’s ability to invest in new startups, as well as those that might be on the cusp of hitting it big.

The $25 million the state planned to use to seed the fund is already in an Elevate Ventures account. The money came from returns earned on investments in early startups Elevate made on behalf of the state—and an IEDC committee has approved its use for the Growth Fund. But Elevate leaders can’t spend any of that money until the organization raises at least some money from outside investors—an effort that could be impacted by the uncertainty about the relationship between the Governor’s Office, the IEDC and Elevate.

“It’s certainly a substantial headwind for them,” said Nick Mathioudakis, a partner at Faegre Drinker Biddle & Reath LLP who advises entrepreneurs.

Still, Mathioudakis said he hopes the Growth Fund will succeed, because it would address a long-acknowledged gap in Indiana’s venture capital landscape.

“I think I speak for a lot of other people in the tech community, where we’re rooting for Elevate,” Mathioudakis said. “I think Elevate is well regarded among the startup community here in town. They’re known, they’re visible, they’re supportive. So most of us are caring and hoping for a positive outcome.”

‘Filling the void’

Announcing the new fund at the Global Economic Summit in Indianapolis in May 2024, then-Gov. Eric Holcomb said the fund would help the state retain young Indiana companies that might otherwise move out of state in search of funding. It could even help Indiana bring companies to the state, the governor said. “This is filling the void that’s been there,” Holcomb said in that May 23 announcement.

Indiana’s then-secretary of commerce, David Rosenberg, and Elevate Ventures CEO Christopher Day were also on hand for that announcement.

“It’s quite a historic moment,” Day then said of the new fund.

In a news release issued by the IEDC the same day as the live announcement, the IEDC said Elevate Ventures would begin forming the fund in the late second quarter of 2024, with a target of starting to make investments from that fund in 2025.

Braun, who won November’s gubernatorial election and was sworn into office in January, is taking a different approach to the IEDC and its affiliates than did Holcomb, a fellow Republican. (Holcomb served two terms as governor and, under Indiana law, was term-limited from running again.)

Citing concerns about transparency at the IEDC and its affiliate organizations, Braun last month announced a funding freeze for Elevate Ventures. The Governor’s Office said it has also ordered an outside audit of the IEDC.

But the Governor’s Office has declined to elaborate on what specifically precipitated the action.

Under its current three-year contract with the IEDC, which runs through June 30, 2026, Elevate Ventures had been receiving $541,667 per month to fund its operations, including staff salaries, programming and other day-to-day expenses. That’s in lieu of more traditional fund management fees and proceeds that Elevate does not collect.

That funding is separate from the dollars the IEDC provides to Elevate—most from federal allotments—to invest in startups.

Fund history

The Growth Fund has been in the works for several years.

At the IEDC’s quarterly board meeting in September 2021, the board unanimously approved allowing Elevate Ventures to reinvest $25 million of the $37 million the organization had earned from investment returns to date.

The full IEDC board was acting on the recommendation of the board’s Entrepreneurship Committee, which had also unanimously approved the idea, meeting minutes show.

Those minutes—which provide a summary of what happened at the meeting but without direct quotes from those who spoke—indicate Elevate Ventures’ then-CEO, Chris LaMothe, told the group that “given the growing maturity of the Indiana investment marketplace, it makes sense to take some of the return dollars and invest them in companies that have moved beyond Elevate’s investment purview.”

The minutes said, “It was recommended to the Entrepreneurship Committee to develop a new fund that would be run by Elevate Ventures which would invest in those later stage companies and hopefully keep them in Indiana as a catalyst to attract other investments.”

Then, in a meeting in November 2024, the Entrepreneurship Committee unanimously approved the creation of the Growth Fund as well as some of the details about how the fund would work.

Specifically, the committee approved using $25 million in investment returns to establish the Growth Fund, “contingent upon Elevate raising at least $50 million in funding from other sources,” the meeting minutes say. That $25 million comes from returns generated from previous investments made by the Indiana 21st Century Research and Technology Fund, the minutes say.

The Growth Fund would target growth-stage companies, and at least $50 million of the ultimate fund would be invested in companies “with a significant presence in Indiana,” the minutes say.

Then, in December, the IEDC’s full board heard a report on the Entrepreneurship Committee’s Growth Fund vote, but the IEDC did not vote on this or any other issue at its meeting, board minutes indicate.

Current status

That $25 million, which comes from returns from Elevate Ventures’ previous investments, is currently sitting in an Elevate Ventures bank account.

But Elevate can’t touch that money until and unless it raises an additional $50 million from private markets, Elevate Ventures Managing Partner Matt Tyner told IBJ during an April 28 interviewew, which took place just days after Braun announced the funding freeze.

“The fund does not exist until we can raise capital from private investors,” Tyner said. “So, even though we have an anchor commitment [the $25 million from Elevate Ventures’ investment returns], it does not get touched until a fund actually exists.”

Since that interview, Elevate officials have declined to respond to IBJ questions.

In the world of venture capital, a fund’s general partner—in this case, Elevate Ventures—raises money by securing commitments from investors. As the fundraising progresses, the fund typically has interim closings, allowing the general partner to begin making investments even if it has not yet raised its full target amount.

For Elevate Ventures and the Growth Fund, that initial close could happen once the fund has $75 million—the $25 million in seed funding from Elevate Ventures and the $50 million from outside investors.

Mathioudakis, the Faegre partner, called the initial close “a magical milestone for any fund” because those first funding commitments are the hardest to secure.

“Once you’ve completed your initial close, a lot of other companies and prospective investors say, ‘OK, now it looks like they’ve gotten to the critical mass,” Mathoudakis said. “And it’s easier for them to follow on and join.”

Mathoudakis is a business attorney who represents both tech companies seeking capital and investors who provide capital. He estimated that he has represented 35-40 clients who have sought investment funding from Elevate Ventures.

In January, Elevate Ventures filed a Form D with the U.S. Securities and Exchange Commission—a standard step in the fund-raising process. In that filing, Elevate Ventures reported that it had not yet raised any money for the Growth Fund. That filing also lists the fundraising target as $200 million—double the $100 million Holcomb had announced a year ago. (In its 2024 annual report, released earlier this year, Elevate Ventures described the Growth Fund as a $150 million fund.)

A different structure

A standard arrangement in the venture world is a fee structure commonly known as “two and 20.” Under that structure, the general partner managing a venture fund receives an annual management fee equal to 2% of the fund’s value. At the end of the fund’s life, investors receive their original investment amounts back. Then, the general partner receives 20% of the profits earned. (The general partner’s cut of the profits is also sometimes called “carried interest,” or simply “carry.”) The remaining 80% of the profits are divided among the fund’s investors.

A simple example: Five investors put in $20 million each, creating an investment fund of $100 million. In each year of the fund’s existence, the general partner receives 2% of that amount, or $2 million, in management fees to pay staff salaries, source deals and do other day-to-day fund administration work. At the end of the fund’s life 10 years later, that initial $100 million investment has grown to $200 million. At that point, each of the five investors receives his or her initial $20 million back. That leaves $100 million in profits. The general partner receives 20% of those profits, or $20 million. The remaining $80 million is split between the five investors.

Elevate Ventures does not use that structure—meaning it does not collect fees or earn carried interest—on its existing investment funds, which are aimed at early-stage companies, where the investments are riskiest. Typically, those are companies raising pre-seed, seed and Series A rounds of funding.

But under the terms set for the Growth Fund, Elevate would collect a 2% management and earn carried interests. The state would not, however, pay Elevate separate management fees for its work on the fund.

Indiana is not unique in wanting to create a public/private investment fund.

“It’s definitely something that states have tried to do to boost the innovation economy,” said Ron Watson, an Indiana native and the founder and CEO of St. Louis-based 1/nCFO. Watson spent about a decade in the venture capital industry, including time at St. Louis-based Lewis & Clark Ventures, whose investment portfolio includes Indianapolis-based health analytics firm Springbuk.

Ohio has such a fund, Watson said, and Missouri also considered launching a public/private fund but did not end up doing so.

In 2023 Watson launched 1/nCFO, which offers fractional chief financial officer services for venture-backed startups.

Watson said the launch of a public/private fund can be a strategy to grow venture funding in states that are far from the coastal hotspots of California and New York.

Typically, Watson said, managers who are trying to raise money for a new investment fund will first go after high-net-worth individuals. Once some individual investments have been secured, the fund then has more leverage with which to convince institutional investors—pension funds, endowments, insurance companies and the like—to also invest.

But securing those initial individual investors is challenging, Watson said, especially for first-time fund managers. “It’s a very difficult game—certainly, if you don’t have that pedigree, it’s tough to do.”

So, Watson said, a public/private fund can be a solution to this challenge: The public funding can be used to kick-start the fund, attracting additional investors to sign on.

What’s next?

It’s difficult to know for sure what the future holds for the Growth Fund.

Elevate Ventures’ Day did not respond to a text message last week seeking updates about what might happen with the Growth Fund.

Governor’s Office spokesman Griffin Reid told IBJ via email last week that there was no new information to share on the Elevate Ventures funding freeze or the audit.

The IEDC did not respond to emails seeking updates, and John Thompson, chair of the IEDC board’s Entrepreneurship Committee, declined to comment.

Watson speculated that Elevate Ventures might target Indiana-based institutional investors—entities that have a natural interest in seeing the state thrive.

“There’s plenty of pension funds and endowments that—they’re very profit-motivated, very return-motivated,” he said. “But they also care deeply about the success of Indiana, and they might be looking for those sort of double outcomes to invest in.”•

Please enable JavaScript to view this content.

Support and funding always differed between a Democratic and Republican administration, but we’ve reached a new level of divisiveness between the MAGAmaniacs and what’s left of GOP.

Indy Innovation Challenge is a $100M IEDC spin off awarded to 3 IEDC officers: David Roberts, Chad Pittman, and Paul Mitchell, since CICP explains they were afraid to lose its non-profit status:

https://opencorporates.com/companies/us_fl/N24000005645

https://projects.propublica.org/nonprofits/organizations/881138295

And apparently the “Innovator Orchestrator” David Roberts perceives himslef as Dave Robertson.

August 2024, Smilodon Capital LLC is registered at 111 Monument Circle, and provides $25M to a new Special Purpose Adquisition Company called Project Energy Reimagined, located at an IEDC Innovation Hub, where David Roberts is the COO, Sponsor, and Capital Partner:

https://lexamples.com/exhibits/contents/NTIwMTE1OA==

Project Energy Reimagined buys an ilegal GM data trader, sued by the State of Indiana for deceptive data practices, called Wejo:

https://businesscloud.co.uk/news/100m-wejo-merger-terminated-still-no-administration/

Project Energy reimagined is accused of stealing $50M from the Bank of China:

https://www.cstonepharma.com/en/uploads/2022/05/165400721280551.pdf