Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe NowHundreds of thousands of Hoosiers will soon be required to make payments on their federal student loans after a 3-1/2-year pandemic pause—and some of those borrowers are more prepared for that day than others.

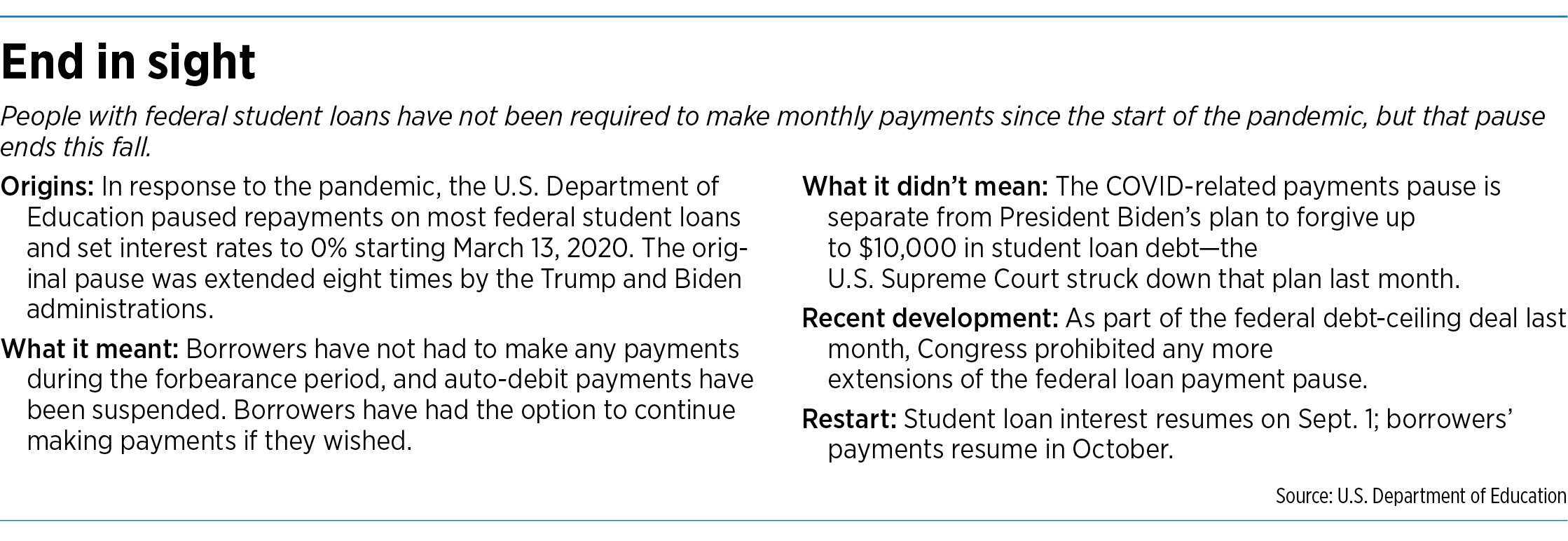

The U.S. Department of Education paused repayments on most federal student loans and set interest rates to 0% in mid-March 2020. That pause was extended eight times by the Trump and Biden administrations, but the forbearance period comes to an end this fall. Interest will again begin accruing on Sept. 1, and borrowers’ payments resume in October.

And, as with so many things related to the pandemic over the past few years, there’s no clear consensus about the impact the resumption of payments could have.

According to U.S. Department of Education statistics, as of March 31, some 921,000 Hoosiers owed a combined $30.5 billion in federal student loan debt. Nationwide, 43.6 million Americans owe a combined $1.64 trillion. Federal loans represent 92.6% of all student loan debt. The remaining 7.4% comes from other sources, including private loans offered by banks or not-for-profit organizations.

“When this all ramps up it’s going to be really interesting because [loan servicing] companies have changed, people have lived life for 3-1/2 years,” said Bill Wozniak, vice president of marketing at Carmel-based INvestEd. “As far as I know, there’s never been anything like this.”

INvestEd offers free financial aid assistance to Hoosier families, and it is also a provider of private student loans.

Wozniak said his office has fielded calls from borrowers who run the gamut on how prepared they are for the resumption of student loan payments. “Anecdotally, on individual calls, we have had the whole spectrum,” he said.

Facing the ‘Grim Reaper’

Broad Ripple resident Hunter Beale, a 2022 Ball State University graduate, took out $31,000 in loans to help finance his degree in entrepreneurship and innovation, with a minor in construction management.

Beale is currently working as an Orr Fellow, with a job as manager of business strategy at Noblesville-based Indiana Auto Care LLC, which operates 16 Indiana and one Ohio Jiffy Lube oil-change shops. On the side, he’s also working to launch his own business, a company called Simpler Living LLC, through which he plans to offer eco-friendly tiny homes as vacation rentals in Brown County.

Because he graduated during the pandemic pause, Beale hasn’t yet been required to make loan payments. Still, he decided to begin making payments several months ago to get a jump start on his obligations, which he personifies in his mind as a financial “haunting Grim Reaper” looming ever closer.

“That man is coming, and he wants your money that you took from him—and he wants more, because that’s how businesses work,” Beale said.

Beale chose a 25-year repayment plan with $105-per-month payments, though he’s been paying more than the minimum because he said he can afford to. “I’m pretty good with finances and budgeting and being frugal with my money.”

It doesn’t hurt that he makes a good salary as an Orr Fellow, and that since graduating, he’s already built up savings and an emergency fund.

‘A really chaotic process’

Not everyone is so confident about his or her financial situation.

Alexis Merchant, the content and communications coordinator for not-for-profit organization IndyHub, said she anticipates needing to increase her income when her student loan payments resume.

“I’ll have to pick up a second or third job, without a doubt,” she said.

Merchant owes about $25,000 in student loans from her time at Central Michigan University. She attended school there from 2011 to 2012 but did not graduate.

Merchant said she left school with about $32,000 in student loans and had paid between $6,000 and $7,000 of that amount before the pandemic. But she has not made any payments since the pandemic pause began in March 2020. She said over the last few years her income from a contract job and later her own social media company has not always been steady. In April she started her job at IndyHub, which offers professional, social and civic networking opportunities for Indianapolis residents in their 20s and 30s.

During the course of the pandemic, Merchant’s life has changed along with her income. She moved to a new apartment with her fiancé, bumping her monthly housing costs from $800 to $1,250. The couple is also putting money toward their January 2024 wedding.

During the payment pause, Merchant was hopeful that most of her college debt would be erased by President Joe Biden’s debt forgiveness plan, which was struck down last month by the U.S. Supreme Court.

Under that plan—which was meant in part to relieve some burden for borrowers as they eased back into debt payments—those who received need-based Pell Grants would have had up to $20,000 in debt canceled. Other borrowers with annual incomes of less than $125,000 would have seen $10,000 of their debt canceled. Merchant said she would have qualified for $20,000 in forgiveness.

Merchant, who is on an income-based repayment plan, had been paying $350 a month pre-pandemic. Since her income has changed, she is not yet sure how much she will owe per month when repayments resume. She said she’s attempted to call for information three times but hasn’t been able to get through to anyone. “It’s just a really chaotic process,” she said.

Cutting back

Borrower Sam De Elorrieta, who lives in Indianapolis with her husband and daughter, said she expects to pay about $300 a month when her student loan payments resume.

De Elorrieta graduated from Ball State in May 2019 with a degree in business administration and $43,000 in student-loan debt. After a six-month post-graduation grace period, she had just started making loan payments when the pandemic began.

She hasn’t made any payments since March 2020. “I’ve been trying to put that money into savings so that when it starts going to student loans again, it won’t be as much of a hit,” she said.

De Elorrieta works as an associate insurance archaeologist at Indianapolis-based PolicyFind, a firm that finds previously issued insurance policies that can cover current claims.

Like Merchant, De Elorrieta said she was disappointed the Supreme Court struck down the White House’s debt forgiveness plan. “It would have cut my loans in half.”

In the meantime, De Elorrieta said her family might have to cut back on discretionary spending once loan payments resume. That might mean fewer dinners out with friends or weekly ice-cream outings or tackling oil changes at home rather than taking the car to the shop. “We’ll find a way to make it doable,” she said.

The bigger picture

When student loan payments resume, the resulting drop in discretionary income could have a negative impact on the economy, some economists have said.

“It’s a measurable aggravation to the economy, not to mention a measurable aggravation to households,” said Phil Powell, academic director of the Indiana Business Research Center at Indiana University’s Kelley School of Business.

“What’s happening right now in the economy, what’s saving us from a recession, is the fact that households have been spending a lot of money,” Powell said. “They’ve been spending down their excess savings from COVID, and we’re in the last vestiges of those reserves.”

Americans’ cumulative $1.6 trillion in outstanding student loan debt represents about 7% of the country’s GDP, Powell said. Based on his calculations, the resumption of loan payments could slow down the country’s GDP growth by 0.5% to 1% as borrowers divert their budgets from discretionary spending to student-loan payments. GDP growth is currently between 1% and 2%, he said.

Economist Michael Hicks, director of Ball State’s Center for Business and Economic Research, sees it differently.

According to the Federal Reserve Bank of New York, at the end of 2021 Indiana borrowers had an average of $32,045 in outstanding student loans. The median balance for Hoosier borrowers was $17,642. (In comparison, the U.S. average that year was $36,245 and the median was $18,767.)

The median, or the middle number in a group arranged from smallest to largest, is a better measure of the typical debt load, Hicks said. The average is inflated by the relatively few borrowers with the largest outstanding debts, which gives an inaccurate picture of the typical Hoosier’s student-loan debt.

Borrowers in the 22-30 age range will likely see the most impact when student loan payments resume, Hicks said, becaue they are in the time of life when they may be buying their first car or home or starting a family. But for borrowers with less than about $25,000 in debt, Hicks said, “servicing that debt shouldn’t be enough to substantially delay home ownership and that type of thing.”

And, Hicks points out, not everyone has student loan debt. So as for the broader impact of the pandemic pause’s end, he said, “I think it’ll be fairly muted.”•

Please enable JavaScript to view this content.

Debt doesn’t go away – it just accrues interest. Pay what you owe.

Good, get a second or third job to pay for student loans like a lot of us have done in the past. Pay what you took, nobody forced you to go to college.

I’m confused at why so many take out loans and act shocked that they have to actually pay them back. We took out loans for my husband’s career path and from day one everything was planned accordingly. A less than apartment, eating out as a special treat, and vacationing was 13 hour drive to our parents house once a year.

You don’t know the world that you’re living in today. It’s not like what it was when you where growing up.

How is this still a topic of discussion?? And why is this such a big surprise to the individuals, & liberal media, that decided to sit back, relax, and hope for a false miracle to occur that the current administration lied to them about? It is infuriating to hear any kind of sympathy or sentiment towards anyone who borrowed any kind of money that now expects free handouts; a mortgage, credit card debt, student loans, business loan, you name it. Not a single person in this country forced any individual to go out and get a student loan. Not a single person in this country forced any individual to do something they can’t financially afford such as, and not limited to, higher education. What this country is doing is enabling individuals to come to expect handouts and sympathy for things most of us have done on our own before. Where is the sympathy for those of us who have paid off our student debt(s) and made ends meet without expecting others to give us handouts (and no thanks, we don’t want accolades or sympathy for making our own way and contributing to society).

Instead of focusing on the fact that the current administration failed at pushing this utter unconstitutional nonsense through, the media should focus on the massive number of shortages in the trade industry that pays very HIGH wages. Instead of sitting on their couches, collecting government freebies, and waiting for the gates of fake lala money to magically appear, learn a trade, earn a more than respectable living, and pay back what you personally agreed to borrow while leaving all of us alone with this joke.

I think the “bigger picture” is the shear number of people saying they won’t pay a dime when payments resume. Lets discuss the number of people with $1000 in savings (or less) who can afford these student loans. News flash a lot of people can’t.

The system needs broken.

The system definitely has problems. An overhaul of that system should be the priority. Typically, recent college grads are jumping into entry-level positions as should be expected. Many are still living at home. But their expectation is not realistic–they aren’t going to be able to immediately move out on their own into a new home, buy a new car, live the lifestyle of a semi-seasoned professional AND pay back student loans. They need to set their priorities differently. A student loan should not be able to be defaulted on and (in my opinion) lenders should be able to go back to universities and have that transcripts marked as “Void due to withholding of student loan payment” so employers can see the lack of integrity some people have.