Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

In retrospect, Vibenomics Inc. CEO Brent Oakley is really glad the Fishers-based marketing tech company closed on its $12.3 million Series B funding when it did.

Vibenomics closed the deal in May, as the tech sector—and venture investors’ appetite for dealmaking in general—was slowing.

“Thankfully, we did it at that time,” Oakley said. “[The market] was definitely cooling at that time, but we were so far down the process we were able to land the plane.”

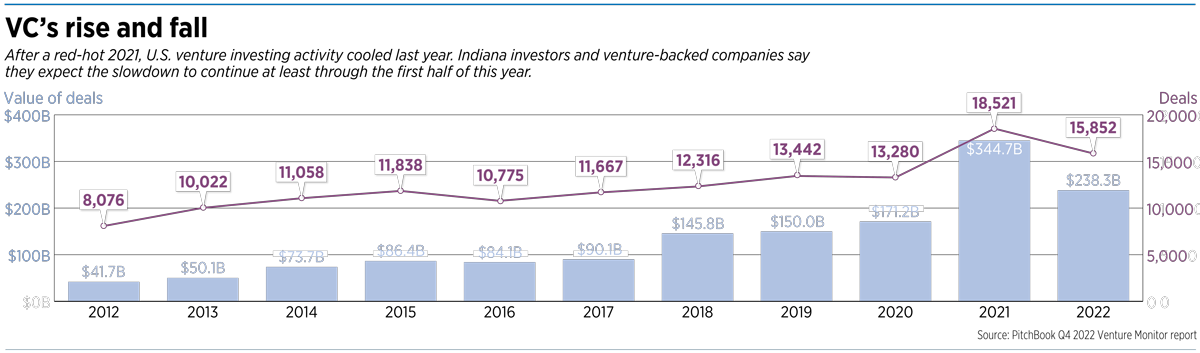

After a red-hot dealmaking environment in 2021, venture investment activity slowed noticeably in 2022. Nationwide, the number and value of deals dropped, company valuations declined significantly, and investors became more discerning in the deals they chose.

It’s an environment that Oakley, and other local venture-backed companies and investors, expect to see carry into at least the first half of this year—maybe longer.

“I think it’s going to be a tough year,” said Seth Corder, a principal at Indianapolis-based venture studio High Alpha. The studio invests in business-to-business software-as-a-service companies in Indiana and elsewhere.

To be clear, deals are still getting done, and local sources see the current slump as a correction following a period of overheated activity. Also: The stats for 2022 deal activity in Indiana outpaced national averages, for a variety of possible reasons.

But firms that make investments in Indianapolis and elsewhere—and local companies with out-of-state investors—say the current deal environment now is markedly different from what it was in 2021 and early 2022.

“Getting cash right now—it’s hard,” said Eric Christopher, co-founder and CEO of Indianapolis-based Zylo Inc. The software firm closed on a $31.5 million round of Series C funding in November.

According to the Seattle-based business data and research company PitchBook, venture investors across the United States closed 15,852 deals last year worth a combined $238.3 billion. That compares with 18,521 deals worth $344.7 billion in 2021.

Indiana saw 176 deals last year worth a combined $743.3 million, up from 162 deals worth $509.1 million in 2021, the PitchBook data says.

And Indianapolis-based not-for-profit Elevate Ventures, which functions as the venture investment arm of the Indiana Economic Development Corp. and invests exclusively in Indiana companies, actually had a record year in 2022.

Elevate Ventures made funding commitments of just over $31 million and closed nearly $21 million in total transactions, said Elevate Ventures Partner Matt Tyner. That’s up from $20 million in commitments and $17 million in transactions the previous year. (Commitment and transaction figures are different, Tyner said, because some of the deals to which Elevate Ventures commits funding don’t end up closing until the following year.)

Tyner said Elevate expects its transaction value this year to be about the same as last year’s.

One reason Indiana bucked the trend in 2022, perhaps, is that many investments here are smaller deals in early-stage companies.

According to data from Indianapolis-based not-for-profit TechPoint, only 6% of tech-sector investments in Indiana last year were late-stage investments. TechPoint defines a late-stage deal as an investment of $10 million or more by a professionally managed fund.

Trickle-down effect

And it typically takes a while for a market slowdown to affect funding for early-stage investments, said Victor Gutwein, managing partner at Chicago-based venture firm M25.

That, Gutwein said, is because market slowdowns typically start among publicly traded companies. When the stock price for those companies begins to fall, the slowdown next moves to large, privately held companies and continues to flow down from there.

Gutwein said he started to see early signs of weakness in late-stage investing activity in late 2021. The slowdown started to affect Series A rounds by spring 2022. Seed funding—smaller investments in early-stage startups—started to suffer by the fall.

The slowdown has definitely had an impact, local VC investors say.

At the height of the market, Corder said, High Alpha was getting deals done in as little as three weeks in cases where the studio was already familiar with the founder and the company. Now, that same deal might take six to eight weeks.

“When everyone was deploying capital at such a quick pace a couple of years ago, there was a lot of pressure to get a deal done,” he said. “Now, there’s not that pressure.”

TechPoint CEO Ting Gootee said she has seen similar trends. “Investors are not in as much of a rush to get a deal done.”

Asking more questions

One effect of that slower pace is that investors have more time for due diligence on potential deals.

For High Alpha, Corder said, that means the studio can meet with more members of a company’s leadership team—not just the founder, but maybe the sales director and other executives—to get more insight into a potential investment target.

Investors are also asking more questions.

M25, which has made a dozen investments into Indiana-based companies, has been asking for more details about companies’ founders and customer bases, Gutwein said.

Specifically, he said, M25 is more interested now in founders’ experience levels, and in the stability of a company’s customer base. “Are they customers that are likely to go out of business or cancel?”

M25 is an investor in Indianapolis-based Authenticx, which this month announced it had closed on a $20 million Series B round—its second major post-seed-stage funding. Authenticx is a business communications software company that focuses on the health care and insurance industries. Its customers include health insurers, health care systems, hospital systems and pharmaceutical companies.

“Their customers are name-brand health care customers that are not going to go away,” Gutwein said of Authenticx.

Likewise, investors are more focused now on capital efficiency and steady, predictable growth, Zylo’s Christopher said. “This is the new investor mindset.”

Zylo, which launched out of High Alpha in 2016, offers a platform to help customers analyze and manage their software-as-a-service subscriptions.

Christopher said Zylo has been prudent in its spending, avoiding the growth-at-all-costs approach taken by some other tech firms, particularly those on the coasts.

“Eighteen months ago, that wouldn’t have been very exciting” to investors, Christopher said. But he believes that measured approach is one reason Zylo was able to land significant funding even as the markets have tightened.

Return to Earth

Another significant deal-making shift since 2021: Company valuations are down dramatically.

Traditionally, Corder said, software companies based in the Midwest have had valuations of eight to 10 times annual revenue. Those valuations rose to as high as 15 to 20 times revenue, Corder said, and in a few cases coastal tech firms achieved valuations as high as 100 times revenue.

Valuations have since declined about 50%, returning to near or at their previous norms, Corder and others said.

Valuation is important in the venture investing world because a company’s valuation affects existing investors’ equity in the company. As an example: An investor who puts $1 million into a company worth $10 million has a 10% ownership stake in that company. But if the company’s valuation drops to $5 million, a new investor would receive a 20% stake for a $1 million investment.

A company’s valuation is also a signal to the market, Gootee said, and a drop in valuation is a negative signal. So, if a company is trying to raise money based on a lower valuation than in previous rounds, she said, potential investors will want to know why.

Making the money last

Faced with the realities of a down market, companies now need to make their investment capital last as long as possible.

“Everybody has longer runway expectations,” Gutwein said.

In the VC world, the term runway refers to the amount of time before a company needs to raise more capital.

During the boom, Elevate Ventures’ Tyner said, companies might be able to get away with needing to raise money every 12 to 18 months. Now, investors—Elevate Ventures included—want to see that runway extended to 18 to 24 months.

“You want as much time for the market to turn around as possible so that you don’t find yourself raising money twice in a down market,” Tyner said.

Putting it in starker terms, Oakley said he would advise other venture-backed firms, “Whatever you do, you can’t run out of money today. It’s always been the rule of CEOs, but it’s never been more important to not run out of money.”

“If you have to raise money now, the cost of money is so expensive for you as a founder,” he said.

Vibenomics is an audio marketing tech company. Its technology, voice talent and licensed music library allow customers to deliver music, audio advertising and messaging to their in-store shoppers. The company’s list of customers includes the Kroger and Hy-Vee supermarket chains.

Vibenomics has been able to keep its costs in line without resorting to layoffs, Oakley said. But the company has slowed its growth plans. When it closed on its Series B funding in May, the company had close to 40 employees and told IBJ it planned to increase that number 25% by year’s end.

But Vibenomics hit the brakes on those hiring plans. Oakley said the company now has 41 employees.

Looking ahead, sources offer differing views on how long it might be before the funding slump eases.

Oakley believes the down market could last through the end of next year, but others are more optimistic.

Tyner sees the market bottoming out this summer before beginning to improve. But he’s not totally confident about that. “I think the question that no one has a good answer for yet is how long it will take to recover.”•

Please enable JavaScript to view this content.

Editor's note: You can comment on IBJ stories by signing in to your IBJ account. If you have not registered, please sign up for a free account now. Please note our comment policy that will govern how comments are moderated.