Subscriber Benefit

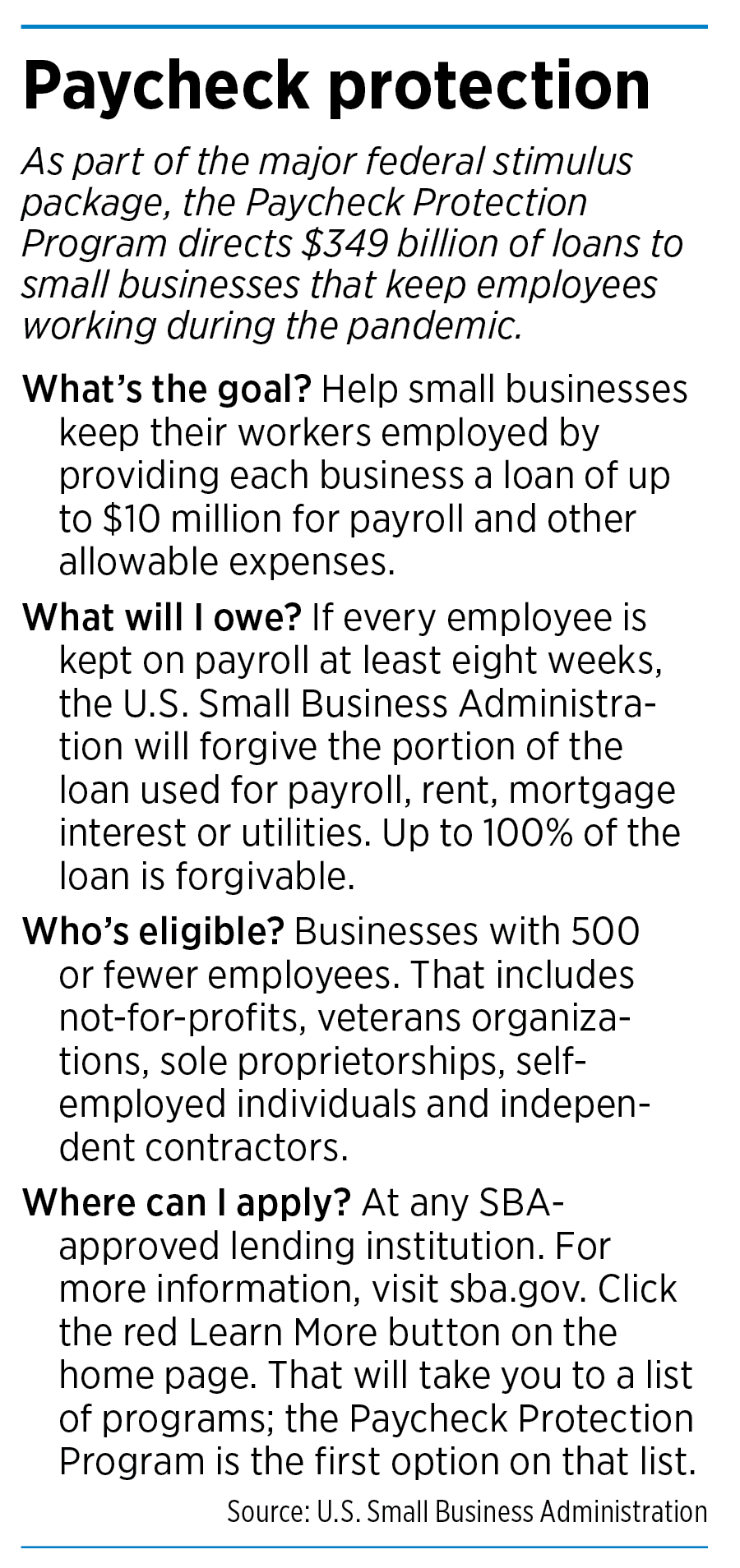

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe NowNearly $350 billion in forgivable federally backed loans could be a lifeline for small businesses and their employees amid the COVID-19 outbreak—and under current guidance, nearly every small business in Indiana could qualify, experts say.

Last week, Congress passed the Coronavirus Aid, Relief and Economic Security Act, the third federal stimulus package approved by lawmakers in the wake of the economic fallout related to the pandemic.

Beyond individual stimulus checks for Americans, one of the CARES Act’s most anticipated programs is the Paycheck Protection Program, a federally guaranteed loan program that gives small to medium-size businesses the capital experts say they desperately need to survive and continue paying their employees.

The program provides eight weeks of cash-flow help through federally guaranteed loans to small businesses that maintain payroll during the COVID-19 emergency. Most notably, loans used to cover payroll costs, interest on mortgage obligations, rent and utilities can be forgiven.

Small businesses could receive money as soon as April 3, the Associated Press reported. That prediction came from senior administration officials who said companies would be able to submit applications on Friday. Money could become available to borrowers the same day.

The final rules that will govern the loan program had not been finalized by press time, but that had not stopped businesses from preparing their applications. Banks, tax advisers and the Indy Chamber are already fielding inquiries from small businesses seeking the aid.

“Business owners are facing a lot of difficult decisions,” said Ian Nicolini, vice president of Indianapolis economic development for the Indy Chamber. “And having access to capital that doesn’t require collateral allows them to focus on business decisions and not considerations they would make around their real estate holdings or personal finances.

“This really intends to get businesses through this hibernation period.”

The loans can be for up to 2-1/2 times the borrower’s average monthly payroll costs, up to $10 million. For employers, qualifying payroll costs cover the gamut, including basics like salaries, wages and commissions, but also payments for cash tips, for vacation or family leave, for health care benefits, retirement benefits and more.

Interest rates can be no higher than 4%.

Matt Whiteside, the co-founder and CEO of Circle Kombucha, is eyeing the Paycheck Protection loan program as a way to keep his employees on the payroll, even as production of the company’s fermented tea drink has shut down.

Matt Whiteside, the co-founder and CEO of Circle Kombucha, is eyeing the Paycheck Protection loan program as a way to keep his employees on the payroll, even as production of the company’s fermented tea drink has shut down.

He said the program is an appropriate role for government to play, given it required so many companies to shutter operations.

“Stimulus in a format like that drives the right behaviors,” Whiteside said. “It’s not a free handout. You have to bring your people back on payroll. You have to meet certain criteria. But if you meet those things and the loan can be forgiven, I think that can really help the economy get back up and going again.”

The CARES Act makes a wide swath of businesses and not-for-profits eligible for the program, including those with fewer than 500 employees, individuals who operate as independent contractors or who are self-employed, and most veterans organizations.

And to help the hard-hit restaurant industry, the 500-employee rule is applied on a per-physical-location basis. For businesses that operate as a franchise or received financial assistance from an approved Small Business Investment Company, normal affiliation rules that can limit SBA aid eligibility don’t apply.

The program is an extension of the SBA’s 7(a) loan program, and the loans will be administered by banks and other lending institutions approved by the U.S. Department of Treasury or the SBA.

Nicolini said the loans are designed to be accessible. Lenders will want to ensure that businesses are seeking the loans only to deal with the current economic uncertainty and that the money will be used to retain workers and maintain payroll or to make mortgage, lease and utility payments.

“For businesses that are going to keep employees and cover operating expenses, it’s a really useful loan product because it’s administered to banks, so it can be deployed relatively quickly,” Nicolini said. The loans are “up to $10 million, which is sizable, and then the portions related to paying payroll and benefits are forgivable.”

But not everyone is so sure.

The American Hotel and Lodging Association, for one, has argued that providing companies—especially hospitality companies—with loans equal to 2-1/2 times monthly payroll won’t be enough to keep the doors open.

“This [funding] is an insult,” said Sanjay Patel, president of Indianapolis-based MHG Hotels, which owns 16 properties across the country, including five in central Indiana.

“They’re putting in nails into coffins,” Patel said. “If somebody takes this money, they’re buying the nail [and] their coffin.”

Business interests worried about a provision in an early version of the federal legislation that would have prohibited businesses from applying for the Paycheck Protection Program if they already had applied for an Economic Injury Disaster Loan, a program the SBA offered early in the crisis. But that provision was eliminated in the final bill.

As a result, emergency loans made to businesses after Jan. 31 will be rolled into the Paycheck Protection Program.

To ensure that more businesses are eligible, no collateral or personal guarantees are required, and lenders won’t consider whether the borrower sought credit elsewhere and was denied, the U.S. Chamber said.

Already, Indy Chamber has fielded hundreds of calls and messages from businesses asking about loan products, Nicolini said. The chamber recommends businesses start with their banks to get an idea of what they could be approved for, the time frame for receiving the loans and more.

To provide even more help, the chamber and the city have partnered to provide businesses with micro rapid-relief loans of $1,000 to $25,000 that can be issued on top of other options. Some of the federal loans could take weeks to be issued, so the rapid-relief loans can serve as bridge financing, Nicolini said

“We’re trying to serve a niche that is additive to what the banks are offering,” he said. “I would encourage businesses to have the conversation with their bank first and check out the resources that we have. If they don’t have a relationship, or they’ve got a longer lead time for when they might be able to access capital, we could be a resource.”

Meanwhile, the tax services group of Katz Sapper & Miller has already started working with its clients to assemble documentation they might need to apply for the Paycheck Protection Program loans.

Chad Halstead, partner in KSM’s Tax Service Group, told IBJ that, although small businesses have a few options in COVID-19 relief programs, the Paycheck Protection Program is likely to be the most sought after because it’s forgivable.

Small businesses that need the loan should begin by talking with their banks, accountants or legal counsel as soon as possible so they’re prepared to apply, he said. SBA guidance could be handed down to banks in as soon as a few days.

“The influx of applicants here [is] going to be more than you can possibly imagine,” he said. “I can’t overstate how many folks are going to apply for this loan.”

Halstead is encouraging his clients to have historical information about their businesses handy and to begin accumulating the documents they’d need for a typical loan application. Some banks are already allowing businesses to get in line for applications, he said.

“The word of advice is, if this is something you want to do, you want to get an application in as soon as possible because I think there’s going to be a long queue of applicants,” he said. “If the cash is really important to you, you want to be in the front of that line.”•

Please enable JavaScript to view this content.

Just to make sure I understand this program correctly – tax payers are basically paying to run small businesses for the next 8 weeks? Also, does this mean that employees at these businesses can’t collect unemployment because they are still being paid?